Economic Growth

Economic activity decelerated sharply in Sub-Saharan Africa in 2016 to an estimated 1.3 percent growth, its worst outcome in more than two decades. This low growth rate was driven mainly by unfavorable external developments, with commodity prices remaining low, and difficult domestic conditions. Angola, Nigeria, and South Africa experienced a marked slowdown in economic activity. A decline in oil production halted economic growth in Angola. In Nigeria, gross domestic product (GDP) contracted by 1.5 percent amid tight liquidity conditions, budget implementation delays, and militant attacks on oil pipelines. Growth in South Africa weakened to 0.3 percent, reflecting contractions in the mining and manufacturing sectors and the effects of the drought on agriculture. Excluding these three countries, growth in the region was estimated to be 4.1 percent in 2016.

Other oil exporters struggled to cope with a large terms-of-trade shock, as activity contracted sharply. Metals exporters fared relatively better, as they benefitted from the large drop in oil prices. Nonetheless, output levels and investments in the mining sector were also hit hard and budgetary revenues fell. Average growth among the non-resource-intensive countries remained high in 2016, reflecting their more diversified economies. Growth in these countries was partly supported by scaled-up public infrastructure investment.

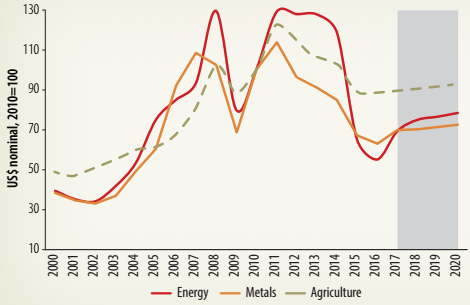

Sub-Saharan Africa is seeing a recovery of growth in 2017. Rising commodity prices, strengthening external demand, and the end of the drought in several countries are among the factors contributing to the rebound. Prices of most commodities continued to rise in early 2017, from their lows in early 2016 (figure 1.2). The oil price increase in 2017Q1 reflects steady demand growth and the agreement between some OPEC and non-OPEC oil producers to limit output. However, persistently high global oil inventories along with an improved supply outlook by the in the U.S. shale oil sector, impose constraints in the longer term price outlook of oil prices. Metals prices are strengthening, partly reflecting increased demand from China. Meanwhile, above-average rainfalls are boosting agricultural production in countries that were hit by the El Niño-related drought in 2016 (South Africa, Malawi).

| Security threats subsided in several countries. In Nigeria, the decline in militants' attacks on oil pipelines has helped oil production to rebound. The slowdown in Angola, Nigeria, and South Africa-the region's three largest economies-appears to have bottomed out toward the end of 2016. Non-resource-intensive countries, including those in the West African Economic and Monetary Union (WAEMU), have been expanding at a solid pace. | FIGURE 1.2: Commodity Price Forecast

Source: World Bank. | Prices of most |

Several factors are preventing a more rigorous recovery in the region. In Angola and Nigeria, restrictions on access to foreign exchange continue. Although the Central Bank of Nigeria and the National Bank of Angola have recently increased the sales of foreign exchange in the interbank markets, foreign exchange liquidity conditions remain tight, and are holding back activity in the non-oil sectors. The manufacturing and services sectors remain particularly weak in both countries. In South Africa, policy uncertainty and low business confidence continue to constrain investment. Unemployment remains very high. The recent (April 2017) downgrade of the country's credit rating to sub-investment level by Standard and Poor's and Fitch is likely to weigh on the country's economic prospects (box 1.1).

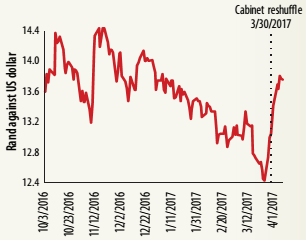

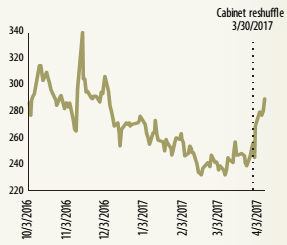

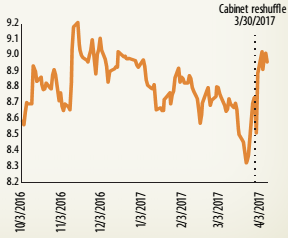

| BOX 1.1: | A controversial cabinet reshuffle by President Zuma on March 30 prompted Standard and Poor's to quickly (April 3) downgrade South Africa's long-term foreign currency debt rating to sub-investment grade-the country's first "junk" grade since 2000. Within a few days (April 7) of this rating action, Fitch downgraded local and foreign currency debt to sub-investment grade. These rating moves reflect mounting concerns about policy and institutional uncertainty in the country. | |

| Most of the economic effects of the rating slippage are still evolving. Thus, the focus of this box is on (a) describing some of the channels of transmission of this event in the short term, and (b) reporting on the immediate effects that are observed in foreign exchange movements and borrowing costs in debt markets. Recent studies have examined what a rating downgrade could mean for the South African economy (Hanusch et al. 2016; World Bank 2017). A decline in ratings implies a higher risk premium on debt. Broadly, the potential channels through which a rating shock affects the economy in the short run are by (a) raising the cost of borrowing and servicing debt; (b) increasing net capital outflows, as investors reassess risk (including institutional investors, who are reluctant to hold sub-investment grade assets), putting downward pressure on the exchange rate; and (c) increasing inflationary pressures from exchange-rate pass-through. The economic impact of a decline in sovereign rating will depend on whether the downgrade reflects new information on economic fundamentals and country risk. Often, rating changes are viewed as lagging the market, in which case the actual rating event might elicit little response. The monetary and fiscal policy response will shape outcomes as well, especially in the long term. Short-Term Effects How did the market variables react? Anticipating a downgrade, several market indicators had already started weakening: the South African rand lost 7.9 percent during March 27-31, sovereign bond spreads ticked up 30 basis points, and the 10-year local-currency bond yields rose 52 basis points (figure B1.1.1). The size of the pullback in the currency is larger than the decline of around 5 percent experienced in the immediate aftermath-that is, within two days-of the Brexit surprise. Markets continued to weaken in the wake of the downgrade announcements of April 3 and 7. In the two weeks ending April 7, the rand had depreciated by a cumulative 10.7 percent, sovereign bond spreads had risen by 50 basis points, and the 10- year local currency bond yields had increased by 59 basis points. These indicators are now at levels comparable to those in late December 2016, when expectations of a rating downgrade were rife. Although it remains to be seen how the policy framework and governance issues will evolve, the recent events represent a setback to business and investor confidence, and are likely to weigh down on the country's prospects. | FIGURE B1.1.1: Evolution of Market Indicators South African Rand against USD

| |

| EMBI Sovereign Spreads

| ||

| 10-year Bond Yields

| ||

Elsewhere in the region, several oil exporters in the Central African Economic and Monetary Community (CEMAC) are facing difficult economic conditions. The contraction of activity that began in the oil sector in Chad, Equatorial Guinea, and the Republic of Congo has spread to the rest of the economy. Although the economies of Cameroon and Gabon have not contracted-due in part to their relatively more diversified exports-activity has slowed notably and oil production continues to decline. Having delayed the adjustment to lower oil revenues, CEMAC countries are now embarking on fiscal tightening to stabilize their economies. In Chad, the ongoing fiscal adjustment has entailed significant reductions in recurrent and capital expenditures, which weakened domestic demand. Elsewhere, in Mozambique, the recent government default and debt burden are deterring investment. The drought in East Africa, which reduced agricultural production at the end of 2016, has continued into 2017, adversely affecting activity in some countries (for example, Kenya) and contributing to food insecurity in others (Somalia, South Sudan) (box 1.2).

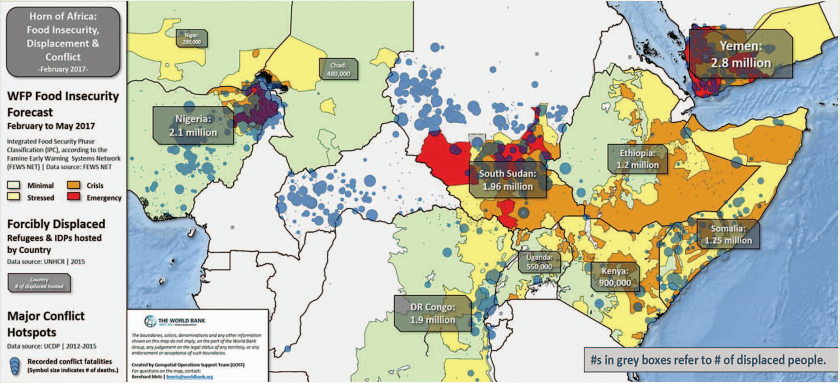

| In 2016, rains failed across large swaths of countries in Eastern and Southern Africa. Although weather shocks are not uncommon in Africa, the 2016 drought stands out in scale and severity, because of the unusually large number of countries announcing significant drops in the levels of crop production, especially of staples, at the same time. For example, maize production in 2015/16 in the 15 member countries of the Southern African Development Community (SADC) fell by an average of 19 percent compared with the 2014/15 maize season. Similarly, in Eastern Africa, severe crop and livestock production losses were reported, especially in the Horn of Africa. The drought also led to power disruption, depressed economic activity, and increased poverty. Drought-induced declines in maize were estimated to reduce gross domestic product in the SADC area by 0.1 percentage point, and increase poverty by 1.4 million people. This particular drought is blamed on one of the strongest El Niño (and sister phase La Niña) effects in memory. That said, droughts need not lead to famines. Rather, famines occur when households with depleted own resources are unable to access food because of public (government or community) inaction or willful neglect. Public inaction may be due to lack of financial resources or bureaucratic capacity to deliver needed food to the affected population. However, it could also be due to toxic politics that trigger conflicts or neglect the suffering of supporters of political opponents. In short, famines are almost always due to government failure. In early 2017, a famine was declared in South Sudan by the United Nations, and a pre-famine alert was issued for Somalia; there is a food crisis in northeast Nigeria (map B1.2.1). Whatever the cause of famine may be, it leaves scars in the short and long terms. The most painful short-term consequence of famine is increased mortality, which results from a sustained period of increased food insecurity, a time when affected populations, especially children, are deprived of basic nutrition for months. MAP: B1.2.1: Conflict Leads to Food Insecurity and Complicates Response

An estimated 260,000 people died from the 2010/11 famine in the Horn of Africa. In 2016, an estimated 250,000 South Sudanese children under the age of 5 were estimated to suffer from severe acute malnutrition. An equally visible consequence of famine is forced displacement. Displacement may be a natural response by affected populations to move to "security" (where food and physical protection are available) or flee the environment that is threatening their lives. For instance, it is not uncommon that, during severe droughts, one group of herders competes for pasture and water with another, during which conflict and displacement ensue. Prices are also likely to spike, make food unaffordable, and exacerbate malnutrition. Although not immediately obvious, the long-term consequences of famines, especially on human capital, have been shown to be serious. Epidemiological studies of famine-affected populations have shown that famines cause psychological disorders, obesity, glucose intolerance, and blindness due to deprivation of vitamin A. Other studies that look at the impact of in-utero exposure to famines show that they lead to lower height, which has been shown to be a good indicator of long-term health and educational outcomes. These disadvantages in human capital, in turn, have led to lower prospects in the labor market-lower productivity, lower wages and earnings, and higher poverty. As past and recent outbreaks of famine have shown, a reduction in conflict will almost certainly lead to fewer future famines. In addition, automatic stabilizers, such as safety net programs, which could be scaled up in the event of severe droughts, are necessary even for poor countries. Functioning markets are just as necessary, to provide price stability and affordability and accessibility to food. Finally, even under conditions where conflict is absent, markets work, and safety net programs exist, the ability and efficiency with which to prevent famine for many countries is hamstrung by nonexistent or unreliable data. Therefore, building a credible early warning system is crucial to prevent future famines. Such a system would include data on living conditions, vulnerability, and livelihoods that are collected by national statistical offices and geospatial and satellite-based remote sensing data, and capacity to analyze and forecast. Cheap early warning systems in this age of the digital revolution are affordable and transformational for many poor countries. However, to take full advantage of these technologies to prevent famine, most poor countries are better served by investing in centers that receive satellite imagery from the multiple satellites that circle the African skies, and building the capacity to analyze such images to forecast crop failures and droughts. | BOX 1.2: |

Annex 1A examines the behavior of growth, capital accumulation, and productivity after a commodity price plunge. Overall, the analysis finds that vulnerability to shocks represents a substantial cost in output and productivity for countries in the region. The challenge for resource-abundant countries is to go beyond capital accumulation, to formulating policies to boost productivity and the efficient allocation of resources within and across industries.