Outlook

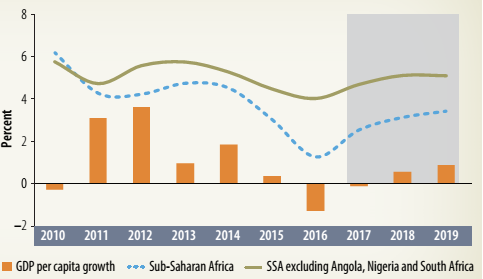

Growth in Sub-Saharan Africa is forecast to pick up to 2.6 percent in 2017, rising to 3.2 percent in 2018 and 3.5 percent in 2019 (figure 1.7). The turnaround is predicated on the projected rise in commodity prices (box 1.3) and policy actions to tackle still-large macroeconomic imbalances in several countries. The forecasts are weaker than those in October, reflecting a more moderate recovery among metals exporters and a muted recovery in growth in South Africa. Non-resource-intensive countries are expected to continue to expand at a solid pace. Overall, growth is projected to rise only slightly above population growth, a pace that is largely insufficient for creating employment and supporting poverty reduction efforts in the region.

• Growth in South Africa is projected to recover to around 0.6 percent in 2017, rising to 1.1 percent in 2018 and 2 percent in 2019. Weaker growth of private consumption and investment is expected to offset a rebound in net exports, as the sovereign rating downgrade to sub-investment level raises borrowing costs.

| Growth in | FIGURE 1.7 :Growth Prospects of Sub-Saharan Africa

Source: World Bank. Note: GDP - gross domestic product. | For Nigeria, growth is projected to rise from 1.2 percent in 2017 to 2.5 percent in (2018-19). The modest turnaround will be underpinned by a gradual rebound in oil production and an increase in fiscal spending. |

In Angola, growth is projected to increase from 1.2 percent in 2017 to 1.5 percent in 2019, spurred by a modest increase in oil production. In Nigeria and Angola, recovery in the non-oil sector will be constrained by foreign exchange restrictions and high inflation. The subdued outlook for Angola, Nigeria, and South Africa implies that per capita output will decline in these countries over the forecast horizon.

• Growth will be weaker than previously projected in the CEMAC area, as oil production increases at a slower pace than previously projected, due to maturing oil fields in several countries, and fiscal adjustment reduces public investment. In metals exporters, high inflation and tight fiscal policy will be a greater drag on activity than previously expected in several countries.

• Growth in non-resource-intensive countries should remain robust, based on infrastructure investments, buoyant services sectors, and the recovery of agricultural production. Ethiopia and Tanzania in East Africa, and Côte d'Ivoire and Senegal in WAEMU will expand at a solid pace, although some of these countries may not reach the high growth rates of the recent past. Growth is projected to strengthen in Ghana, as increased oil production boosts exports.

| According to the World Bank's Commodity Markets Outlook, oil prices are expected to average $55/barrel in 2017, up 28 percent from 2016, as the stock overhang is expected to unwind during the second half of 2017. Oil prices are projected to average $60/barrel in 2018. There are considerable risks (especially downside) to the oil price forecast. Key among them is the resilience of the U.S. shale oil industry. Indeed, the U.S. Energy Information Agency reported higher than expected output in its March report, which was the key cause of the weakening in oil prices in March. On the upside, disruptions among politically stressed producers (Iraq, Libya, and Nigeria) or an extension of OPEC cuts into 2018 could exert upward pressure on prices. Average annual prices of metals and minerals, which declined 6 percent in 2016, are projected to rise 11 percent in 2017 and 1 percent in 2018. Price forecasts have been increased since January due to stronger than envisioned demand in China and some unexpected supply constraints. Agricultural prices are projected to remain broadly stable in 2017 and 2018. The stock-to-use ratios of the three key grains (maize, rice, and wheat) have reached 15-year highs, while supplies of other food commodities (such as edible oils) are adequate. Since agricultural production is energy intensive, lower costs due to lower energy prices (compared with pre-2015 levels) continue to have a dampening effect on grain and oilseed prices in 2017. In addition, lower energy prices reduce the incentive to divert land use away from food to biofuel commodities. | BOX 1.3: |

Underlying the outlook, lower inflation is expected across most of the region. The recovery of agricultural production, following the end of the drought, will help reduce food price inflation in several countries, including South Africa. Reduced inflation will allow central banks to loosen monetary policy. However, inflation is expected to remain elevated in Angola and Nigeria throughout the forecast horizon, reflecting limited adjustment in the foreign exchange market. Drought conditions remain in parts of East Africa-notably Kenya-and will exert pressures on inflation in these countries this year. Fiscal and current account deficits are expected to improve somewhat for commodity exporters, helped by the continued recovery of oil and metals prices and some reduction in fiscal spending. In non-resource-intensive countries, the fiscal and current account positions are likely to remain under pressure as countries struggle to strike a balance between the need for fiscal consolidation (Kenya, WAEMU) and public infrastructure investment spending.