Slowdown in Investment

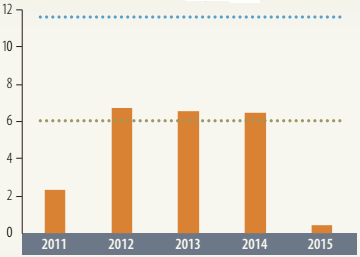

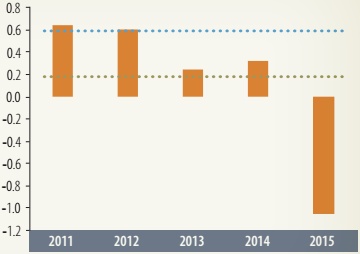

The low growth in Sub-Saharan Africa is reflected in part in the investment growth slowdown the region has experienced. Investment growth in the region slowed from nearly 8 percent in 2014 to 0.6 percent in 2015, well below the long-term (1990-2008) average of about 6 percent and the fast-paced growth of 11.6 during 2003-08 (figure 1.9). The sharp drop in investment growth in 2015 is evident across public and private investment. The deceleration in investment growth has pulled down the share of investment in GDP by 1.05 percentage points, reversing the cumulative gains in this measure over the three previous years.

Investment growth has slowed sharply, pulling down the share of investment in GDP. | FIGURE 1.9: Trends in Investment Growth (%) Investment growth

|

Changes in Investment to GDP

|

|

Source: International Monetary Fund Investment and Capital Stock Dataset, 1960-2015. | |

Given the large investment needs of the region, increasing public investment will be a priority. Public investment directly boosts overall investment in the economy and can foster private investment. But few countries in the region are well positioned to ramp up public investment. Most countries have little fiscal space to increase public investment, because of their high debt-to-GDP ratios and the need for fiscal consolidation. External financing conditions have tightened with increased uncertainty in the United States and Europe, which makes tapping debt markets increasingly difficult and risky. At the same time, in many countries, low tax revenues, weak banking systems, and underdeveloped capital markets limit the share of domestic resources that can be allocated to public investment. In low-income countries, regulatory and implementation capacity constraints are key obstacles to scaling up public investment in infrastructure.

Four key areas of policy priorities to address investment needs and ensure sustainable financing are the following:

• Sustaining public investments. Domestic resources-tax and nontax revenue-are likely to remain the dominant source of financing for infrastructure. Increasing domestic revenue may provide the most sustainable way to finance infrastructure investment. This will require improving tax collection as well as cost recovery. In many countries, debt levels are still manageable, and borrowing to increase spending on infrastructure remains a viable option. However, debt sustainability should not be compromised.

• Encouraging greater private sector participation in infrastructure. Countries need to strengthen the pipeline of bankable projects that can meet the financial objectives of private investors. Innovative fund and deal structures, such as guarantees and risk sharing, should be developed to mitigate risk. Blended finance instruments that can leverage private sector development financing should be promoted. Public-private partnerships (PPPs) are a tested strategy that can be applied to many sectors. However, governments must establish autonomous regulatory agencies to oversee private agents. The terms of the partnerships must be monitored carefully to ensure that PPPs deliver a normal return and not a monopoly profit.

• Strengthening public investment management systems. Effective public financial management capacity is critical for scaling up infrastructure investment spending. Countries should seek to strengthen the capacity for project selection and appraisal, and enhance the monitoring of project execution to minimize leakages. Operation and maintenance expenditures for existing infrastructure should be fully integrated into a medium-term expenditure framework to ensure that they receive adequate budgetary resources.

• Promoting regional integration of infrastructure. A regional approach to the provision of infrastructure services is needed to overcome the region's geographic and physical challenges. This will require effective regional institutions, setting priorities for regional investments, harmonizing regulatory frameworks and administrative procedures, and facilitating cross-border infrastructure.

These issues are discussed in more detail in the special topic of this report (section 2).