Rising Debt

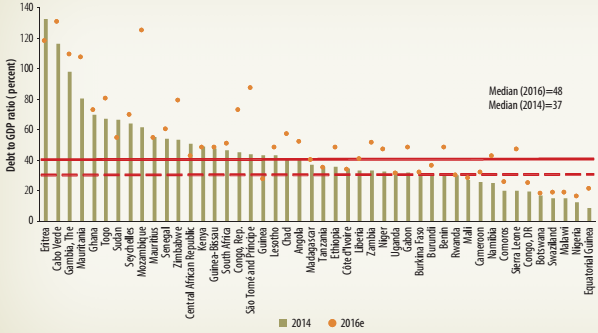

Debt levels are on the rise in Sub-Saharan Africa and, in some cases, rapidly. Public debt in the region has continued to rise amid large/widened fiscal deficits and weak growth. The median general government gross debt-to-GDP ratio stood at 48 percent in 2016, more than 10 percentage points above the level in 2014. But there is wide variation across countries. For the bottom quartile of countries in the region, general government gross debt is less than 40 percent of GDP; for the top quartile, it exceeds 60 percent of GDP.

Debt ratios among oil exporters have increased by about 15 percentage points of GDP over the past three years (2014-16), to a median value of 50 percent. Among non-resource exporters, Mozambique has public debt levels exceeding 100 percent of GDP, after information exposed government guarantees on debt by several state-owned enterprises (figure 1.11). Other countries have borrowed to finance much-needed infrastructure programs-for example, Ethiopia, with the second phase of the Growth and Transformation Plan.

| Of 46 countries in the region (excluding South Sudan and Somalia due to lack of data), the debt ratios of 44 countries changed during 2014-16. Of the 35 countries with rising debt ratios, 18 saw at least a 10-percentage point increase in this ratio between 2014 and 2016. | FIGURE 1.11: Public Debt-to-GDP, Countries in Sub-Saharan Africa, 2014 and 2016

Source: Macro Poverty Outlooks, Africa Region, World Bank 2017. | Debt ratios among oil exporters have increased by about 15 percentage points of GDP over the past three years. |

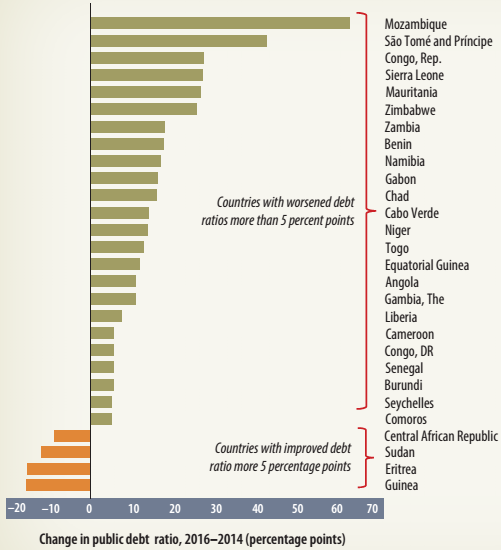

In six of these countries, the increase was greater than 20 percentage points: Zimbabwe, Mauritania, Sierra Leone, the Republic of Congo, São Tomé and Principe, and Mozambique (figure 1.12).

| Public debt levels are sustainable to the extent that the funds borrowed generate returns that allow timely repayment. However, some countries in the region are caught in an environment of low growth prospects, widened fiscal deficits, weaker currencies, and lower export revenues, and could face problems in repaying their debt. | FIGURE 1.12: Change in the Public Debt-to-GDP Ratio between 2014 and 2016, Selected Countries in Sub-Saharan Africa

Source: Macro Poverty Outlooks, Africa Region, World Bank 2017. | Zimbabwe, Mauritania, Sierra Leone, the Republic of Congo, São Tomé and Príncipe, and Mozambique have seen their debt to GDP ratio increase by more than 20 percentage points. |

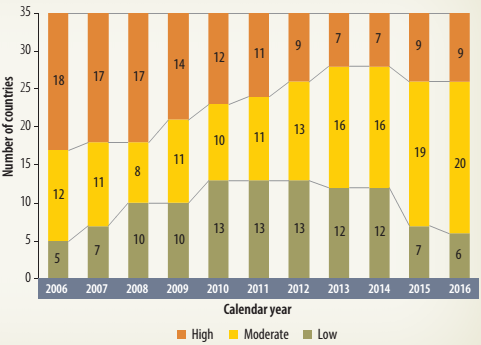

At the same time, normalization of monetary policy in the United States and credit rating downgrades in some African nations (for example, Angola, Mozambique, and the Republic of Congo) have raised borrowing costs for countries in the region. Among 35 low-income and lower-middle-income countries in the region, the number of countries with low risk of debt distress declined from 12 in 2014 to six in 2016 (IMF-World Bank Debt Sustainability Analysis) (figure 1.13).

| Among low - and lower - middle-income countries, the number of countries with low risk of debt distress declined from 13 in 2012 to six in 2016. | FIGURE 1.13: Evolution of the Risk of Debt Stress: Low-Income Countries in Sub-Saharan Africa

Source: International Monetary Fund/World Bank, Debt Sustainability Analysis database, February 2017. | In an environment with tighter and more volatile global financial conditions, many countries in Sub-Saharan Africa face the challenge of undertaking their muchneeded development spending without jeopardizing their hard-won debt sustainability. This will require not only conducting sound and sustainable monetary and fiscal policies, but also developing local currency bond markets. |

The ability of governments to issue debt in their own currency will reduce their dependence on external funding and, more importantly, exposure to exchange rate risk. At the same time, public bond issuances may gradually shift from short-term and floating debt to fixed rate debt, thus reducing the exposure to interest rate fluctuations. The capacity of debt management organizations across countries requires upgrading as well.