Public-Private Partnerships in Sub-Saharan Africa

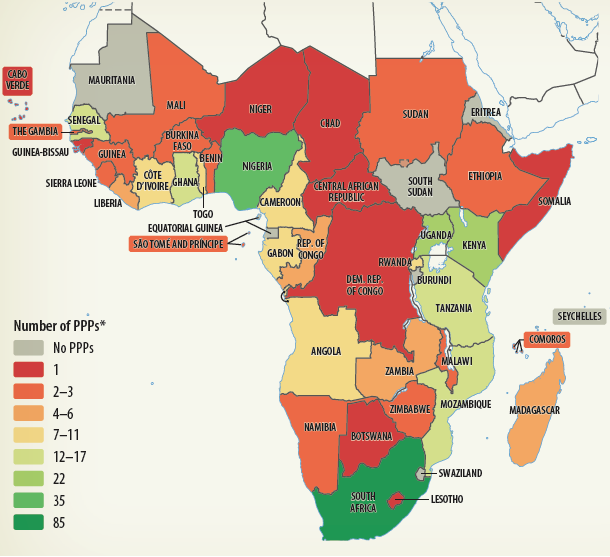

Amid heightened interest in crowding-in private investment, there is renewed interest in public-private PPPs. PPPs in Sub-Saharan Africa remain a very small market. The development of PPPs, which has been slow, started in the early 1990s, beginning with projects in South Africa and Cote d'lvoire in 1990. Eventually, PPPs spread to 41 of the 48 countries in the region, most recently Botswana and Somalia in 2011 and 2013, respectively. Burundi, Eritrea, Eguatorial Guinea, Mauritania, the Seychelles, South Sudan, and Swaziland do not have any PPPs. According to the World Bank's Private Participation in Infrastructure (PPI) database, there are 335 PPPs18 in infrastructure19 projects in Sub-Saharan Africa that have reached financial closure20 in the past 25 years.

| However, the entry year is not the best indicator of how active each country is in bringing PPP projects to the market. Despite that many countries in Sub-Saharan Africa started early, they never produced another PPP after their first one-for example, Central African Republic (1991), Guinea-Bissau (1991), and the Democratic Republic of Congo (1995). | MAP 2.2: Number of PPP Projects by Country (1990-2015)

Source: World Bank PPI Database, February 7, 2017. *Note: Number represents unique projects per country. Cross-border projects are counted once for each country. | Countries with the most projects in the region are South Africa (85 projects), Nigeria (35), Kenya (22), and Uganda (22). |

The most active countries in the region are South Africa (85 projects), Nigeria (35), Kenya (22), and Uganda (22) (map 2.2). Nine countries have only produced one PPP, and another 13 have produced only two or three in the past 25 years. The low number of PPPs in these countries can be attributed to the fact that some are small economies; others have been in conflict for several years; or they have weak legal and regulatory frameworks for procuring and implementing PPPs.

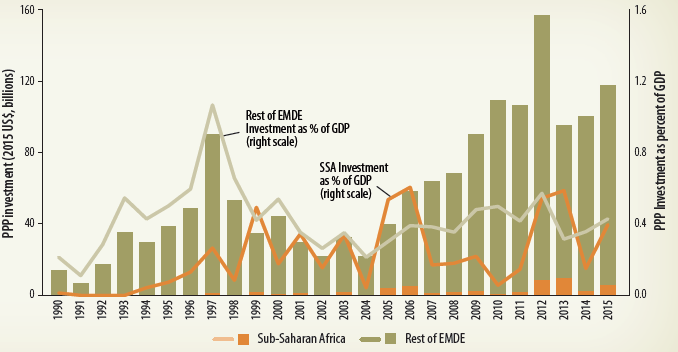

Overall, the number of PPP infrastructure projects in the region is a relatively small proportion of the total number of projects in emerging markets and developing economies (EMDEs), ranging from 2 to 12 percent.21 Because the proportion is so small, in figure 2.42, the scale for the number of projects in Sub-Saharan Africa has been expanded; the right scale shows the fluctuations over the years. Although growth has been evident in the past 25 years, it has been somewhat less pronounced in Sub-Saharan Africa than in the rest of the EMDEs, with slightly more volatility as well.

This pattern also holds when we look at PPP investment commitments in Sub-Saharan Africa, which make up only a small portion (2-10 percent) of total EMDE investment. When adjusting the data by the size of the economy, it can be observed that before the Asian financial crisis (1997-98), PPP investment as a percentage of GDP was clearly below the average for the rest of the EMDEs, reaching a peak of 0.2 percent in 1997 compared with 1.1 percent for the rest of the EMDEs (figure 2.42). However, after the Asian financial crisis, investment as a percentage of GDP fluctuated between 0.2 and 0.6, closer to the average for the rest of the EMDEs.

| PPP investment commitments in the region are a small portion of total investment in emerging markets and developing economies. | FIGURE 2.42: PPP Investment in Sub-Saharan Africa versus the Rest of the EMDEs |

|

Source: World Bank PPI Database, February 7, 2017. *Note: % of GDP for rest of EMDE uses GDP for all countries except Sub-Saharan Africa. Data exclude telecom, divestitures, merchants, and management and lease contracts. |

___________________________________________________________________________________________

18 A PPP is defined as "any contractual arrangement between a public entity or authority and a private entity, for providing a public asset or service, in which the private party bears significant risk and management responsibility."

19 Infrastructure refers to the energy, transport, and water and sanitation sectors, as defined by the PPI database (www.ppi.worldbank.org).

20 The definition of financial or contractual closure varies among types of private participation as a result of the availability of public information. (a) For management and lease contracts, a contract authorizing the commencement of management or lease service must be signed with the private consortium assuming the operation of the services. (b) For brownfield concession projects, contractual closure is reached when the concession agreement is signed and the date for taking over the operations is set. (c) For greenfield projects, financial closure is the date whereby (i) there is the existence of a legally binding commitment of equity holders and/or debt financiers to provide or mobilize funding for the full cost of the project; and (ii) the conditions for funding have been met and the first tranche of funding is mobilized. If this information is not available, the construction start date is used as an estimated financial closure date. (d) For divestitures, the equity holders must have a legally binding commitment to acquire the assets of the facility. Such commitment usually occurs at the signing of the share purchase contract.

21 This includes all IDA, International Bank for Reconstruction and Development (IBRD), and IDA-IBRD blend countries.