Financing of PPPs

Financing structure. PPP financing may come from public, private, or development finance institution (DFI) sources. Public source financing includes (a) governments providing part of a project's upfront capital costs through grants or viability gap funding (government subsidies24); (b) state-owned enterprises investing equity; and (c) state-owned banks extending loans Private source financing includes equity (including equity financed by corporate debt) through the project's developer, or project finance debt through private lenders, which can be commercial banks or institutional financiers. DFIs also provide various forms of support in the form of loans and equity.

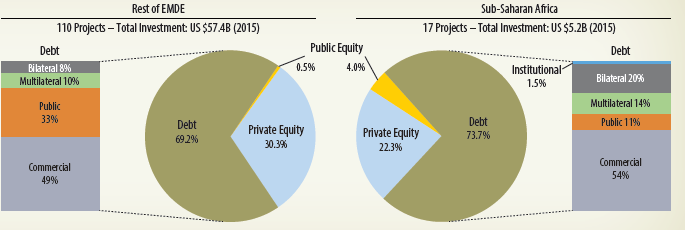

There are limited data on financing for PPP projects in Sub-Saharan Africa. In 2015, there were 334 projects for all countries in EMDEs, 24 of which were in Sub-Saharan Africa, and only 17 of those have complete financial information. The data that are available, however, show that the projects in Sub-Saharan Africa are financed in a very similar way to those in the rest of the EMDEs. In general, projects are financed with about 70 percent debt and 30 percent equity, most of which is private (figure 2.47). There is a slight variation in the debt structure between EMDEs and Sub-Saharan Africa. In both cases, debt tends to be about half commercial, but in Sub-Saharan Africa international financial institutions play a larger role in financing the other half, about 34 percent as opposed to only 18 percent in the rest of the EMDEs, where public debt plays a larger role.

| Most projects are financed with about 70% debt and 30% equity, most of which is private | FIGURE 2.47: Sources of PPP Financing in Sub-Saharan Africa, 2015

Source: World Bank PPI Database, February 7, 2017. *Note: Each category makes up 100%. Data exclude telecom, divestitures, and merchants. |

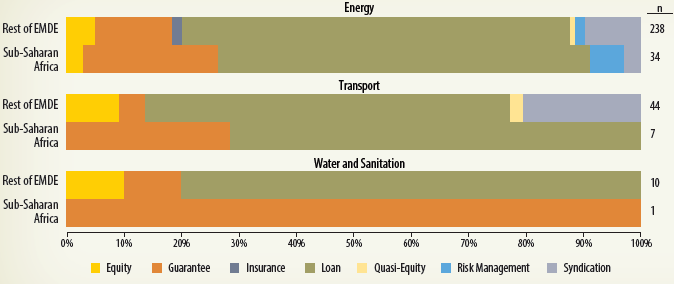

MDB support. Multilateral development banks (MDBs) have helped to facilitate, prepare, and structure complex PPPs to mobilize private sector and institutional capital, and they have helped expand the pipeline of bankable infrastructure projects. The PPI database defines MDB support as financial assistance to the project company, including loans,25 guarantees,26 equity, quasi-equity,27 syndications,28 and risk management instruments. 29 In the past five years, 31 (25 percent) of the 126 projects in Sub-Saharan Africa received some type of financial backing from MDBs, mainly in the form of loans (27 projects) and guarantees (11). This is almost twice as high as the figures for the rest of the EMDEs, for which only 12 percent (213/1,909) of projects have MDB support. 30 In the energy sector, MDBs also provide equity, syndication, and a slightly higher proportion of risk management instruments in Sub-Saharan Africa than they do in the rest of the EMDEs. In the rest of the EMDEs, MDBs contribute more equity in all sectors, some insurance in the energy sector, and syndication in the transport sector. For water and sanitation, there were only three projects between 2011 and 2015, only one of which had MDB support in the form of a debt/equity guarantee-the Befesa Desalinization Plant in Ghana (figure 2.48).

| FIGURE 2.48: Types of Multilateral Development Bank Support for PPPs (2011-15) Sub-Saharan Africa versus Rest of EMDE

Source: World Bank PPI Database, February 7, 2017. *Note: Data exclude telecoms, divestitures, and merchants, and are limited to projects with available information. n = 262 projects. ** The number of observations for each category is greater than the sum of the projects, because it is common for a project to have multiple types of support. | In the past five years, 25% of the PPP projects in Sub-Saharan Africa received some financial support from MDBs.

|

Government support. When projects are not funded through user fees, power purchase agreements (PPA), or water purchase agreements (WPA) with private entities or wholesale markets, governments must support the deals through fixed and variable payments from their budget31 (direct support). In some cases, governments can offer indirect support through guarantees to reduce specific project risks-for example, payment, revenue, and exchange rate guarantees.

In Sub-Saharan Africa, 91 of the 334 projects have information on government support. Of these projects, 46, or 50.5 percent, have some form of government support: four of those received direct government support and the rest, 42, received only indirect support. Of the projects receiving direct support, three received a capital subsidy, and only one received a revenue subsidy. Of the 42 projects receiving indirect support, for 38 it was in the form of a payment guarantee (37 were energy projects); three received a debt guarantee; and only one received a revenue guarantee. Projects in Sub-Saharan Africa tend to receive less government support than those in the rest of the EMDEs, with most of the support in Sub-Saharan Africa going toward payment guarantees, which are most typical for energy projects.

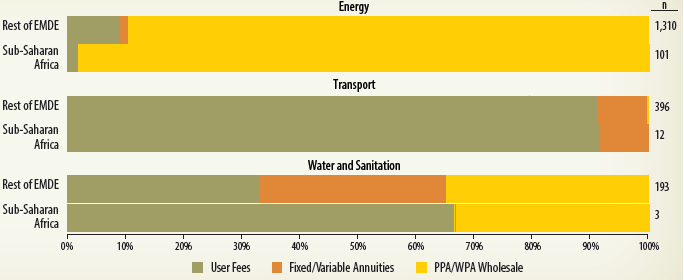

Revenue sources. The sources of revenue for a project can be grouped into three categories: (a) user fees,32 (b) power or water purchase agreements (PPA or WPA)33 and sales to wholesale markets,34 and (c) annuity/ availability payments from the government. In the last category, the government makes direct transfers in the form of fixed or variable payments.35 Very few projects in Sub-Saharan Africa require fixed or variable annuities as a source of revenue (figure 2.49). This is not surprising, since the PPPs in the region are concentrated in the energy sector, which demands PPAs, but it is surprising in the water sector, because there were only three water projects with available information (see n to right in the figure).

| Very few projects in Sub-Saharan Africa require fixed or variable annuities as a source of revenue | FIGURE 2.49: PPP Main Revenue Sources by Sector (2011-15) Sub-Saharan Africa versus Rest of EMDE

Source: World Bank PPI Database, February 7, 2017. *Note: Data exclude telecoms, divestitures, and merchants, and are limited to projects with available information. n = 2,015. |

Cancelled projects. Cancellations have taken place. Although cancelling a project is a last resort, it can still have a meaningful impact on the PPP market. From 1990 to 2015, relatively few infrastructure projects witnessed the exit of a private investor before the contract ended. Although rare, such cancellations can have a sustained impact on a country's PPP program, reducing the private sector's confidence in the government's commitment, as well as the government's confidence in the robustness and "value for money" of these arrangements.

Of the 5,456 infrastructure projects reaching financial closure in EMDE countries during 1990-2015, 204 were cancelled,36 accounting for 3.7 percent of all projects and 5.7 percent of investment commitments. Sub-Saharan Africa shows only a slightly higher PPP cancellation rate (4.2 percent) compared with the rest of the EMDEs, which is mostly due to a higher cancellation rate of 10 percent in the water and sanitation sector (three of 29 projects). The three cancelled projects were all management and lease contracts.

___________________________________________________________________________________________

24 The term government subsidies here refers to all cash subsidies provided by a government for capital investments of a project to cover the costs of the physical assets during construction.

25 Direct loans using multilateral institution funds (also referred to as A-loans).

26 Guarantees include political risk coverage and partial credit guarantees, which turn medium-term finance into a longer-term arrangement by guaranteeing longer maturity or offering liquidity guarantees in the form of put options and take-out financing.

27 Quasi-equity includes both debt and equity characteristics, and some of them are convertible debt, subordinated loan investments, and preferred stock and income note investments (also referred to as C-loans).

28 A multilateral institution arranges the financing with the resources of other investors, but the institution is always the lender of record (also referred to as B-loans).

29 Risk management products, or derivatives, allow project companies to hedge currency, interest rate, or commodity price exposure. Some of them are currency and interest rate swaps, options, and forward contracts and derivatives.

30 There is limited information on projects that do not have MDB support and projects for which we have no information. For this reason, only relative comparisons should be made, on the assumption that research rigor and availability of data are the same in Sub-Saharan Africa and the rest of the EMDEs.

31 In some cases, the government may collect user fees but pay availability payments to the private entities bearing the demand risk.

32 When the PPI project relies exclusively or mainly on user fees to cover its cost.

33 In some cases, the government may collect user fees, but the government still bears the demand risk.

34 This includes power/water plants or transmission lines that sell or transport electricity/water to private off-takers. Wholesale markets include cases when outputs are sold to a single buyer or a group of buyers at market prices.

35 This is when the government agreed to make payments to the project company in exchange for the provision of infrastructure.

36 A project was deemed to have been cancelled if, before the end of the contract period, the private company sold or transferred its economic interest in the project to the public sector; the private company physically abandoned the project (such as withdrawing all staff ); or the private company ceased operation or halted construction for 15 percent or more of the license or concession period, following the revocation of the license or repudiation of the contract. A project is also considered cancelled if the host government issued a decree cancelling the project.