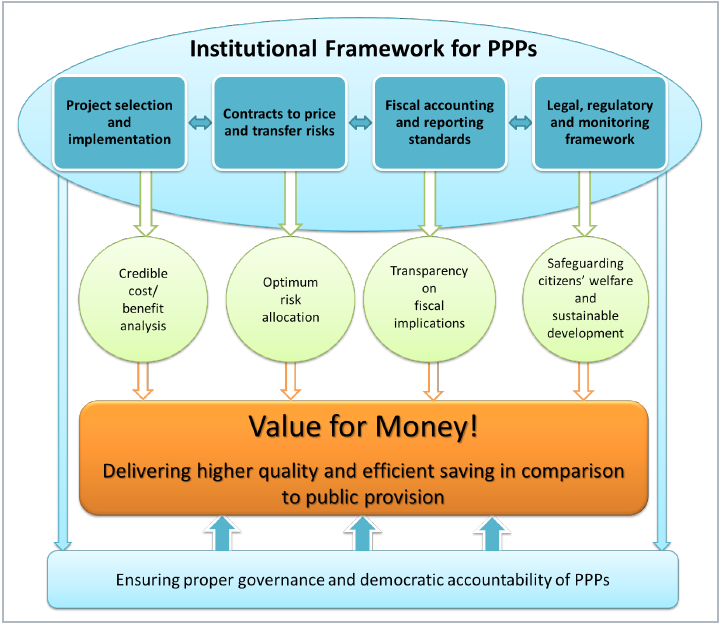

6 The key components of an enabling institutional framework for PPPs

For PPPs to become an effective instrument through improvements in service delivery, efficiency and development impact over and above those attainable through public procurement, it is important that the public sector is able to: i) correctly identify and select projects where PPPs would be viable, ii) structure contracts to ensure an appropriate pricing and transfer of risks to private partners, iii) establish a comprehensive and transparent fiscal accounting and reporting standard for PPPs, and iv) establish legal, regulatory and monitoring frameworks that ensure appropriately pricing and quality of service. In other words, it is necessary that countries have in place the institutional capacity to create, manage, evaluate and monitor PPPs (see Figure 7 for conceptualization).

Taken as a whole, an institutional framework that endows countries with the above four interrelated capacities should have the benefit of ensuring that PPPs are undertaken for the 'right reason', i.e. ensuring an improvement in the quality and cost efficiency of a given infrastructure service to the citizen and not as a vehicle for 'off budget' activities. They are also necessary for making certain that efficiency improvements are measurable and monitored and, broadly speaking, facilitating good governance in the administering of the PPP.

The process of selecting and implementing PPPs is important and should be undertaken on a sound cost-benefit analysis, avoiding any bias in favour of them because they involve private finance. Over-coming planning and project selection problems is critical for reducing the final cost of the project.

The World Bank PPP Reference Guide observes that many infrastructure projects fail due to problems in the planning and selection process: "the analysis underpinning project selection is often flawed, so projects that appeared to be cost-benefit justified turn out not to be so in practice. Benefits are often overestimated, resulting in projects that are larger or more complex than is justified by demand for services, while costs are often underestimated". According to the study by Romero (2015), PPPs can suffer from an 'optimism bias', as a strategic overestimation of demand is common practice. This happens due to weaker incentives for rigorous analysis on both the private and the public sector sides.

Figure 7

Key components of an enabling institutional framework for PPPs

|

|

Indeed, flaws in the project selections can distort the development of public services as PPPs are likely to focus on the most profitable projects. As mentioned earlier, the classic case of such distortions is found in the health sector in Africa where high-tech hospitals in a few urban centres were financed through PPPs even though there are plentiful of wealthy people to support fully owned private hospitals. Thus, the need for universal networks of clinics was ignored. Similarly, in Europe, PPPs often finance some lucrative toll roads on existing busy routes, but not the extension of toll-free roads to improve rural or semi-urban areas.

The setting in train of a credible, transparent and competitive process for the planning and selection of PPPs needs to be accompanied by the structuring of contracts that appropriately price and transfer risks to the private partner. Achieving value for money depends on the ability of the public and private actors to identify, allocate and price risks appropriately. In particular, adequate risk transfer from the government to the private sector is a key requirement if PPPs are to deliver high-quality and cost-effective services to consumers and the government (IMF 2004). Effective transfer of risk, in turn, depends on sufficient competition in both the bidding process and service delivery (OECD 2008). It would also benefit from the establishment of a transparent and comprehensive fiscal accounting and reporting standard for PPPs that would serve to counter perverse incentives that may lead governments to exaggerate or under-state the true value of risk transfer.

By ensuring a transparent and credible evaluation of risks, a comprehensive fiscal accounting and reporting standard would also allow for comprehensive disclosure of all risks, including contingent fiscal liabilities, and thereby enhance the effectiveness of the overall process of selecting and implementing projects. As explained earlier, the fiscal implications of PPPs can arise from non-transparent contingent liabilities (or risk of debts in the future) and can be huge. If a project fails - and this has not been infrequent - the costs are shouldered by the public sector, which has to rescue the PPP project, or even the company, which results in private debts being shifted to the public sector.

Clear fiscal accounting and disclosure of risks would ultimately serve to ensure efficiency gains and value for money by discouraging governments from placing PPP projects off budget and ensuring transparency surrounding the medium to long term implications of the project. However, as mentioned later, there are still no uniform accounting and reporting guideline for PPPs. This is likely to become increasingly problematic as developing countries throughout the world seek to define their own accounting standards for dealing with PPPs. To complicate matters further, practices such as the Eurostat rule adopted in Europe on the criteria to be used to assess risk transfer favour the off-balance sheet accounting of PPPs, which in turn sets a wrong precedent for developing countries not least since a number of European institutions and governments advice on and promote PPPs through their development and investment policies.

Finally, an institutional framework for PPPs should also feature legal, regulatory and monitoring frameworks that allow for the enforcement of contracts, as well as appropriate pricing and quality of service. An enabling legal and regulatory framework would need to ensure a competitive environment during the bidding process and, where possible, service delivery in order to ensure an effective quality of service and allocation of risks. In particular, the broader welfare benefits of projects should be taken into account, including social externalities and the implications for sustainable development. In the case of infrastructure, most projects are natural monopolies that call for external regulation. In such cases, independent and professional regulatory authorities are needed to oversee and monitor the functioning of PPPs (Sarma 2006).

Overall, by strengthening transparency and public scrutiny, and by safeguarding the public interest, an enabling institutional framework with the above-mentioned four interrelated capacities would also serve to reinforce democratic accountability and popular acceptance of PPPs. This has been missing in a number of cases and the study by Romero (2015) illustrates that the lack of transparency and stakeholder participation in some PPP projects has triggered community opposition and unrest. In Peru, for instance, there have been some agreements reached with indigenous communities, but there are also cases where communities have demanded, through mass demonstrations, an open and transparent process of public consultation.

On the whole, efforts to establish an enabling institutional framework for PPPs would require technical assistance and capacity building on the part of the international community in all these areas. It is also necessary to help governments develop the skills needed to manage a PPP programme, and in particular to refine their project appraisal and prioritization. A specific area where global action would be helpful is in the discussion of an internationally accepted accounting and reporting standard which, as mentioned above, can promote transparency about fiscal consequences of PPPs and, in the process, make increased efficiency rather than a desire to meet fiscal targets the main motives for using PPPs. According to IMF (2006), until a common international accounting standard for PPPs emerges, there remains a substantial risk that, in designing PPPs, value for money considerations are traded off against other considerations. This would both defeat the objective of using PPPs for efficiency gains and disguise the medium to long term implications of many PPPs for public finances.

Indeed, all the above issues including consideration of internationally accepted guidelines should be an integral part of future endeavours by the international community committed to hold "inclusive, open and transparent discussion" on guidelines for public-private partnerships, to share lessons learned through regional and global fora.