4.2.4 Financing Real Toll P3 Projects

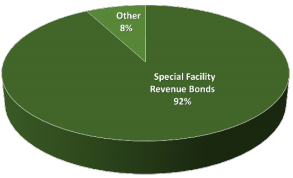

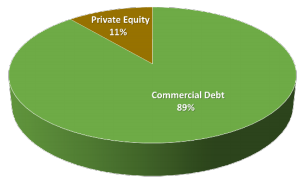

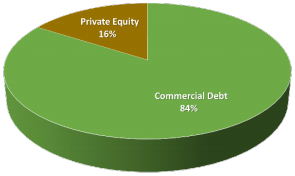

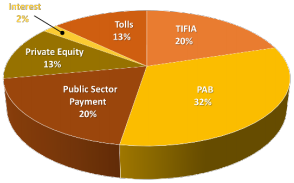

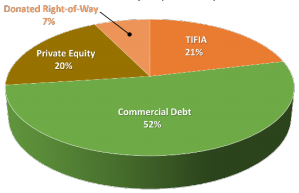

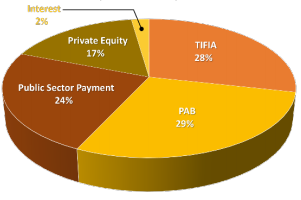

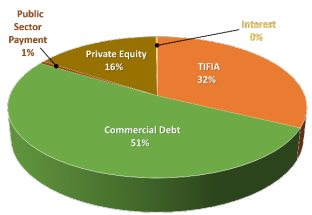

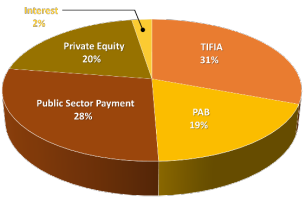

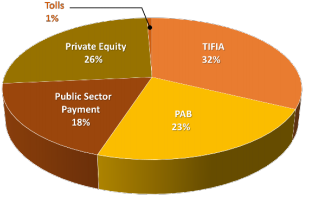

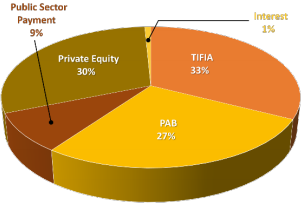

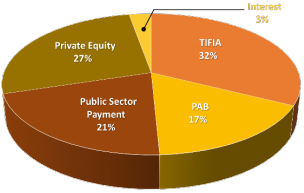

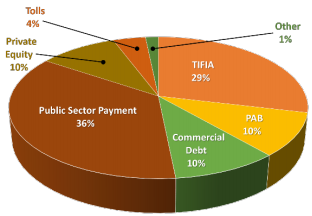

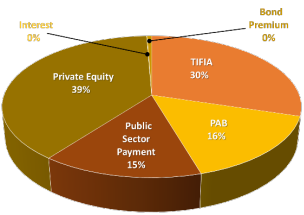

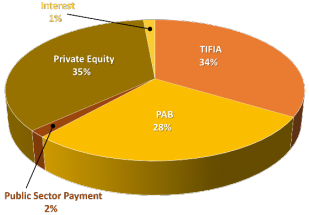

Figure 4-1 provides pie charts identifying the funding and financing sources that have been used on the 14 real toll P3 concessions that have reached financial close in the U.S., together with the percentage of the total project cost they have provided. Each of the 14 real toll projects are presented chronologically. The three real toll projects built in the 1990s predate the establishment of today's federal credit assistance. As a result, P3 developers had limited financing options. For example, the Dulles Greenway and 91 Express Lanes were both originally financed using a combination of commercial loans made by banks and at-risk equity provided by their sector development private partners. The Teodoro Moscoso project involved a one-of-a-kind financing where the government of Puerto Rico used its full faith and credit to raise special facility revenue bonds, which were then repaid by the private partner.

The TIFIA Credit Program was established by TEA-21 in 1998 to provide revenue-generating transportation projects with access to low-cost and flexible financing compared to the terms generally offered by commercial lenders. The goal of the program is to attract private and other non-federal co-investment in transportation projects of regional and national significance. The program was created in recognition of the fact that state and local governments that sought to finance transportation projects with tolls often had difficulty obtaining financing at reasonable rates due to the uncertainties associated with tolling.

As shown in Figure 4-1, TIFIA loans have been used on all 11 real toll P3 transactions to have reached financial close in the United States since the program was established. Beginning with the South Bay Expressway in 2003, the TIFIA program has providing approximately one-third of funding needed to support these projects. The TIFIA credit program was especially helpful to those projects that reached financial close in the wake of the 2008 financial crisis. The most recent real toll P3 project to benefit from the TIFIA Program is the $1.063 billion SH 288 Toll Lanes, which closed on a $357 million TIFIA loan on April 28, 2016.

SAFETEA-LU of 2005 amended Section 142 of the Internal Revenue Code to allow tax-exempt private activity bonds to be used to finance highway and freight transfer facilities. This change allowed private developers lower their borrowing costs by tapping the municipal credit market and gaining access to tax exempt financing. The I-495 Capital Beltway HOT lanes project was the first project to use PAB financing when it reached financial close in 2007. With the exception of SH 130 Segments 5 and 6, PABs have been used on all real toll P3 concessions to reach financial close since the establishment of the program. The combination of PABs and TIFIA financing has enabled real toll projects to proceed in a time of financial turmoil. It has also provided the necessary foundation to leverage other sources of financing, including at-risk equity contributions from private sector P3 investors.

The other major potential credit source for real toll projects is commercial debt. However, banks tend to lend money at a higher cost compared to federal credit programs, as commercial lenders set interest rates to reflect the level of risk involved with each transaction. The risk level is generally documented by ratings assigned to these transactions by the three major bond rating houses: Fitch Ratings, Moody's, and Standard and Poors. Commercial debt has only been used on two real toll projects since the establishment of the TIFIA Credit Program: SH 130 Segments 5 and 6 and U.S. 36 Express Lanes (Phase 2). As discussed earlier, the SH 130 project declared bankruptcy in March 2016, due to lower than expected toll revenues. Commercial debt was a viable financing tool for the U.S. 36 project because it leveraged the toll proceeds from two existing managed lane project, both of which had established and well documented revenue streams. This fact reduced the project revenue risk, allowing the banks to lend money at a more attractive interest rate. The project's risk profile was further reduced because nearly half of its cost was covered by a combination of a public subsidy and private equity.

Figure 4-1: Real Toll P3 Sources of Funding

| Teodoro Moscoso Bridge

| Dulles Greenway

| |

| 91 Express Lanes

| Elizabeth River Tunnels (Downtown Tunnel / Midtown Tunnel / MLK Extension)

| |

| South Bay Expressway

| I-495 Capital Beltway HOT Lanes

| |

| SH 130 (Segments 5-6)

| ||

| North Tarrant Express (I-820 and SH 121/183)

| LBJ Express

| |

| I-95 HOV/HOT Lanes

| North Tarrant Express 35W Project

| |

| U.S. 36 Express Lanes (Phase 2)

| I-77 Express Lanes

| |

| SH 288 Toll Lanes

| ||

Public sector payments have also been an important funding source for several real toll projects. Increasingly, public sector sponsors recognize that large real toll P3 transactions will not be financially viable without their financial participation. Public subsidies can also play an integral role in the adjudication award of real toll concessions. In some procurements, bidders have been asked to specify the amount of the public subsidy that they would need to be able to complete a deal, and in others they are asked to identify the physical extent of a construction program they would be able to deliver with a fixed subsidy. Public subsidies are often used for larger and more expensive projects, such as managed lane improvements that reconstruct entire highway corridors or complex undertakings such as the Elizabeth River Tunnels.

Other sources of funding for real toll projects can include tolls from other existing facilities that the private partner has been asked to operate as part of a concession. Interest payments earned on the proceeds from loans before they are expended or on project reserves can also provide modest amounts of funding for real toll projects.