4.4.2 Financing Long-term Lease Concessions

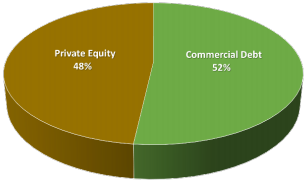

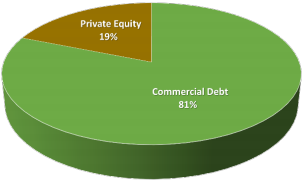

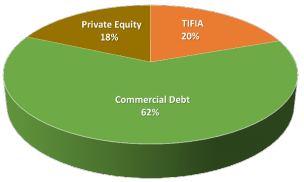

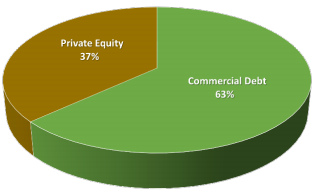

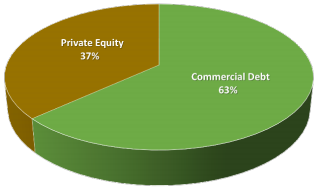

As shown in Figure 4-3, original financings for long-term lease concessions in the U.S. have all comprised significant private equity investment coupled with taxable long-term debt from commercial banks. The fact that these legacy facilities have well established traffic and revenue histories mitigates traffic risk, thereby making commercial debt a viable option for their private sector operators. Given that federal credit programs must be used on projects involving the expansion of existing facilities or the construction of entirely new projects, they have not been available for use on long-term lease projects. The Pocahontas Parkway lease transaction did include a TIFIA loan, which the concessionaire used to help finance the construction of the Richmond Airport Connector.

The percentage of equity as a share of overall concession cost at initial financial close ranges between 18 (Pocahontas Parkway) and 48 percent (Chicago Skyway), with an average of roughly 32 percent. However, the Chicago Skyway concessionaire refinanced its underlying debt only seven months after financial close, reducing its equity share to 25 percent. This change reduced the average level of equity investment for the five long-term lease transactions to 27 percent.

Figure 4-3: Long-Term Lease Sources of Funding

Chicago Skyway

|

| Indiana Toll Road

|

Pocahontas Parkway / Richmond Airport Connector

|

| Northwest Parkway

|

PR 22 and PR 5 Lease

| ||