Project Financing and Implementation

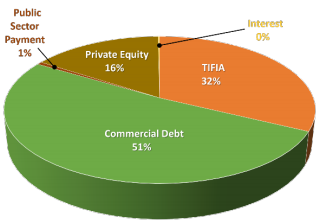

| Following the completion of permitting work for the project, SH 130 Concession Company executed the various loans to raise the money it needed to begin implementing the project. This milestone, known as "financial close," occurred in March 2008. SH 130 Concession Company financed the $1.35 billion project using a combination of loans from commercial banks, a loan from a federal government program known as TIFIA, which provides low-interest and flexible loans to projects of national or regional significance, and its own at-risk equity. | SH 130 (Segment 5-6)

|

The largest single source of financing was $686 million in 25-year loans from a group of five European banks: Banco Santander and Caja de Ahorros y Monte de Piedad de Madrid of Spain, Banco Espirito Santo and Caixa- Banco de Investimento of Portugal, and Fortis Bank of Belgium. The loan is separated into two groups or "tranches": $596.5 million to cover investment needs and $170 million to cover cash flow shortfalls in the first years of operation. During the first five years after construction completion, the loan has a principal payment grace period, which means that SH 130 Concession Company may opt only to make interest payments on the loan.

A $430 million loan from the TIFIA program will be repaid over a 35-year period. The loan is subo rdinated, which means that TIFIA debt service payments will only be made after all debt service on the senior debt held by the five European Banks has been paid in full. The TIFIA loan is secured by a lien on project revenues, with repayments scheduled to begin in 2017 for interest obligations and in 2018 for principal repayments. In addition, a 12-month debt service reserve account will be established beginning in year six of operations and will be in place through the final maturity of the TIFIA loan.

SH 130 Concession Company also has invested $210 million of Cintra and Zachry's own equity in the project. The commercial bank and TIFIA loans will be repaid prior to the company's equity. It is at risk of losing its equity if the project were to default. Cintra and Zachry also provided contingent equity commitments to cover $35 million in right-of-way acquisition costs and $30 million to have additional cash on hand during construction. During construction, TxDOT paid $8 million in compensation to the developer for change orders.

The financing included a $35 million "liquidity facility" from the lending banks that can be drawn on to meet the project's debt payments during the first ten years of operation if needed. If this additional loan is accessed, it will need to be repaid within 30 years.

SH 130 Concession Company completed final design and right-of-way acquisition in early 2009, and construction began that April. The facility opened to traffic in October 2012 and toll collection began the next month. Toll revenues generated on SH 130 Segments 5-6 have fallen well short of expectations, with revenue levels more than 60 percent below original forecasts. As a result, the concessionaire has fully drawn down the bank liquidity facility, and risk ratings on the outstanding commercial bank debt and TIFIA loan have been downgraded to so-called "junk status" by Moody's Investors Service, an important credit rating company. The concession company negotiated with its senior bank lenders to postpone most of its June 2014 interest payment to December 2014, avoiding a legal default. Traffic levels rebounded in 2015, climbing 18 percent in the first quarter of the year compared to 2014. Truck traffic increased by 20 percent. Nonetheless, SH 130 Concession Company filed for Chapter 11 bankruptcy protection in federal court in March 2016. The bankruptcy has no financial impact on the State of Texas, and the operator promises "business as usual for customers, employees, vendors and surrounding communities during [the bankruptcy] proceedings." On September 9, 2016, Cintra relinquished ownership of the facility to its creditors but will continue to operate the facility for 18 months.

TxDOT has retained the right to terminate the CDA with SH 130 Concession Company in the event that the project defaulted. However, TxDOT would be required to compensate the company for its assets at their fair market value. It is unlikely that TxDOT would seek to assume responsibility for the financially troubled facility, as it has no incentive to take on the financial obligations of a toll road with traffic and revenue levels far below projections.

Although the facility was privately funded, TxDOT has invested public resources to promote the toll road. The agency has helped to pay for nearly 400 signs along the I-35 corridor that advertise SH 130 as an alternative route. TxDOT has also paid the concessionaire for providing truck toll discounts as a means to help increase traffic on SH 130 and divert truck traffic from the chronically congested I-35 corridor.