Project Financing and Implementation

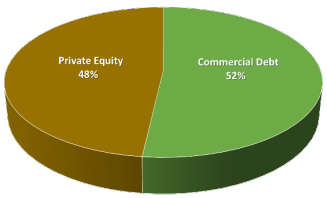

| On January 24, 2005, Cintra and Macquarie reached financial close with their lenders and made a wire transfer of $1.83 billion to the City of Chicago. On January 26, the Skyway Concession Company, LLC assumed operations on the Skyway. The concessionaire originally financed the project with a mix of equity and bank loans. Cintra and Macquarie contributed $485 million and $397 million in equity, respectively, and Skyway Concession Company covered the rest with $948 million in loan proceeds backed by toll revenue. The toll-revenue backed loans were issued by European banks with experience in financing toll roads with taxable debt. They included Calyon (a subsidiary of the French bank Credit Agricole), Depfa Bank of Ireland, and Banco Santander Central Hispano and Banco Bilbao Vizcaya Argentaria of Spain. The bank loans totaled $1.19 billion, were made in nine-year terms, and divided into three parts. The first $1 billion covered the purchase price and the transaction costs, the second part of $110 million covered interest payments during the early period of the loan, and the third part of $80 million covered infrastructure improvements to be made in the early years of the concession. | Chicago Skyway

|

In August 2005, just seven months after financial close, Skyway Concession Company refinanced its underlying debt, raising $1.55 billion in loans and contributing a total of $510 million in equity. By refinancing, Cintra and Macquarie were able to extract $205 million and $168 million respectively in equity from the project and improve their rate of return for investors. Additionally, with their smaller equity investment, Cintra and Macquarie positioned themselves to recover their investment in full within the first 12 years of the concession period, based on forecasted cash flows. After recovery, the concessionaire would be able to operate the facility for the remainder of the concession with no equity risk.

After the repayment of equity to Cintra and Macquarie, $1.016 billion went to refinancing existing bank debt; $36 million was held in reserve, $80 million for expected capital expenditures and $55 million to cover transaction costs.

The $1.55 billion in debt was issued by Citigroup and the four original banks. The debt package was structured in the following manner:

$961 million in capital accretion bonds issued with a 21-year term and a 5.6 percent interest rate. A capital accretion bond is a type of bond where the borrower does not make regular interest payments; instead, the interest is added to the value of the principal and the borrower makes a lump sum payment at the end of the bond's term.

$961 million in capital accretion bonds issued with a 21-year term and a 5.6 percent interest rate. A capital accretion bond is a type of bond where the borrower does not make regular interest payments; instead, the interest is added to the value of the principal and the borrower makes a lump sum payment at the end of the bond's term.

$439 million in current interest bonds issued with a 12-year term. Current interest bonds pay interest at regular intervals.

$150 million in subordinated bank debt. Subordinated bank debt is a type of loan that has a lower credit rating than other debt in a loan package. In the event of a default, creditors with subordinated debt will not be paid until after the senior debtholders are paid in full.

The refinanced debt was rated AAA, the highest possible credit rating, by two large rating companies (Moody's and Standard & Poor's) helping to stabilize and improve the Skyway Concession Company's long-term financial health.

After assuming the operations of the toll road, Skyway Concession Company invested heavily in the modernization of the facility hoping to attract more users, reduce costs and improve operational performance. The company installed the I-PASS electronic toll collection system, significantly reducing peak period congestion at the toll plaza and reducing the Skyway's reliance on manual toll collectors. Once electronic tolling was implemented, 30 percent of peak hour customers shifted from cash payment to I-PASS.

Under the agreement, the Skyway Concession Company immediately increased the toll from $2 to $2.50. After the initial increase, annual toll increases are fixed at 12.5% per year through 2017, when it would reach $5. After the 2017 increase, the toll rate increase is capped at the greater of two percent, the Consumer Price Index or growth in the per capita Gross Domestic Product.

The payment received for the Concession allowed the City of Chicago to establish several funds for city improvements. These funds included:

A long-term $500 million reserve that generates interest income in perpetuity.

A medium-term $375 million reserve that would be drawn down over the course of eight years to provide budgetary relief and mitigate the need to raise taxes in future years.

A $100 million Neighborhood, Human and Business Infrastructure fund that would be drawn down over five years. This fund contributes to over 20 City programs.

In addition, the City used $860 million from the concession proceeds to pay off $390 million in City obligations and $465 million in outstanding Skyway bonds.

Following the Skyway sale, all three credit rating agencies positively revised the City of Chicago's credit outlook. This provided significant long-term benefits to the City, as it reduced the City's borrowing costs on the municipal bond market.