Project Financing and Implementation

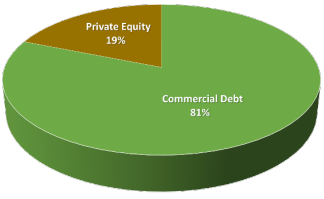

| At the time it reached financial close, the lease of the ITR was the largest private infrastructure transaction in U.S. history. Cintra and Macquarie split their equity share equally, each contributing $374 million toward the lease payment. They financed the remainder with loans from a syndicate of seven European banks, including: Banco Bilbao Vizcaya Argentaria SA, Banco Santander Central Hispano SA, Caja de Ahorros y Monte de Piedad de Madrid, BNP Paribas, Depfa Bank, RBS Securities, and Dexia Crédit Local. The toll receipts from the ITR served as collateral for the debt. The project reached financial close on June 29, 2006, and operations and maintenance responsibilities were transferred from INDOT to ITRCC. | Indiana Toll Road

|

The company's debt package was divided into three parts, or "facilities." It included a $3.2 billion loan used to fund the acquisition of the operating concession, a $665 million "capex" facility to fund capital expenditures through June 2015, and a $150 million liquidity facility. The liquidity facility funded interest payments on the debt and capex facility, and provided a buffer against downward fluctuations in operating cash flows as the concession period began. The financing package also included a fixed-income swap agreement, which deferred most interest payments on the debt and capex facilities until 2015.

During negotiations with ITRCC, the Daniels administration raised toll rates on the ITR but froze further increases until a new electronic tolling system was installed by the concession company. IFA set aside $60 million to compensate ITRCC for the two-year toll freeze. The new tolling system was installed along the full length of the roadway in April 2008. ITR then increased toll rates by 72 percent, although passenger vehicles using an electronic transponder receive a 40 percent discount on the higher rates until 2016. Under the concession agreement, ITRCC had the authority to raise tolls periodically over the life of lease, based on inflation or the rate of national economic growth, whichever was greater.

The concession agreement included minimum operating standards, such as pavement smoothness and landscaping upkeep. The agreement included a 55-year non-compete clause to protect concession revenues. The clause prohibits the state from building or improving any limited-access highways over 20 miles long within ten miles of the ITR. If such improvements are made, the state is required to compensate the concession company for any loss in revenue.