2.4. O&M Costs

| The other component of cost is the O&M cost. This normally includes direct costs and overheads. Overheads reflect the expenditure for administration, management, risks and profits. Direct cost is the cost of inputs such as labour or material, which is determined by the cost of construction and the economic and market conditions. |

|

Each design/engineering option set out in the technical feasibility study would have an O&M cost associated with it. O&M costs would be the recurring expenses that are to be incurred during the project period/concession period.

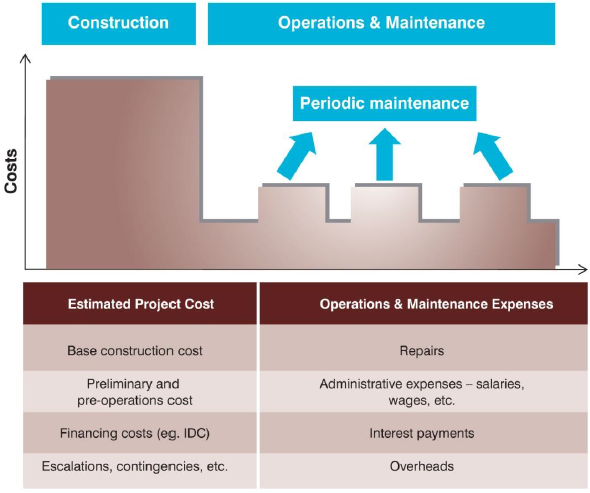

The figure below indicates the capital and O&M expenses for a typical road project.

| Indicative O&M costs in a bulk water supply system project • Establishment charges • Administrative charges • Power cost • Chemicals and consumables • Repairs and replacements |

It may also be necessary to disburse the capital cost of a project in phases whereas O&M costs would usually exhibit a linear or block increase. In the case of a water supply project, the population increase in the region exhibits a linear growth whereas the capacity augmentation is required in phases (for example, in a block of ten/fifteen years depending on the project period, size and scale of infrastructure).

In the case of a metro project, rolling stock is added at specific time intervals, leading to block increase in both capital and O&M expenditure.

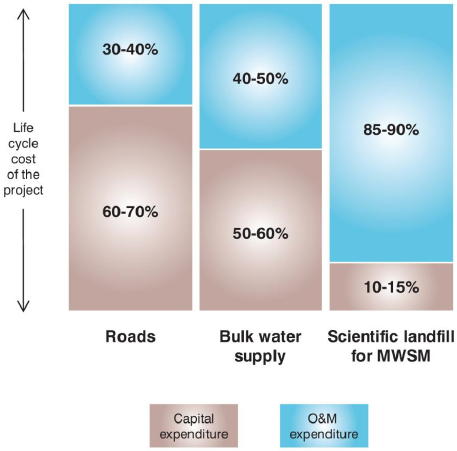

The figure below sets out an indicative share of the capital and O&M expenditure during the project life cycle period, for development of roads, bulk water supply systems and the development of scientific landfill projects.

Reliable cost estimates pertaining to construction, operation and maintenance and the project details, which are set out in the feasibility studies provide a key input to finalizing the bidding documents for the project and enable private entities in submitting realistic bids.