4.2. Project Risks - Retained and Transferable Risks

| To arrive at the PSC, the risks that are present over the life of the project need to be quantified. These include those risks that are retained and those which could be transferred to the private partner. The value of project-specific risks is to be added to the cash flows while calculating the PSC. |

|

The risk may be quantified in terms of a regular cash-flow item or it may be reflected as a discount factor while arriving at the NPV value. Valuing risk in the cash flow of the PSC has the following advantages:

1. Optimal level of risk allocation is comparatively easy to achieve

2. Cash flow valuation takes better account of the timing of risk

3. The value and impact of a particular risk may vary over time;

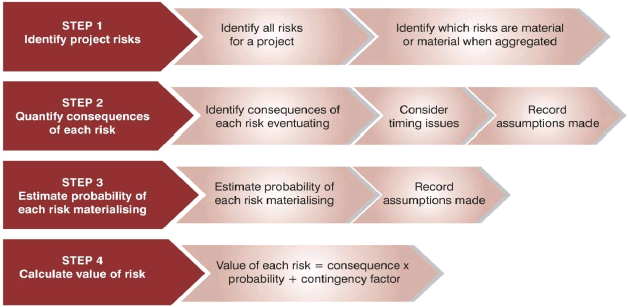

It provides a transparent methodology by using a consistent Government discount rate across projects. The steps in quantifying the risks are explained in the chart below.

A PPP reference bid is a hypothetical private party bid which meets the defined output specifications (the same as that used in constructing the PSC). It is also known as a shadow bid. In this case, the costing of the output specifications should be carried out from a private party's perspective. Comparing the net present cost of a risk-adjusted PSC model with the net present cost of a risk adjusted PPP reference model to the public entity/public finances enables an assessment of whether service delivery by the Government or by a private party yields the best value to the public entity.

Since the public entity may not be able to estimate the costs associated with the output specifications to be charged by the private parties, the transaction advisor should have the necessary expertise, market knowledge and experience to construct a market related PPP reference project in the following stages:

• Determine the nature of the PPP arrangement

• Determine the proposed project structure and sources of funding

• Identify the core components of the payment mechanism

• Estimate taxes accruing to public finances

• Allocate risks

• Assess the value of the transferred risk

• Assess retained risks

• Calculate the net cost of the PPP reference bid