1. Introduction

| Decisions to invest in projects are based on an analysis of the costs and the benefits that accrue from it. Both the private partner and public entity rely on these calculations for decision-making. It is, therefore, necessary to understand the basic principles of cost/benefits analysis for investment appraisals. The investment rationale for the private partner stems from cash flows estimated in the financial analysis:

|

|

| While the public entity also undertakes an assessment of the financials, the investment rationale goes much beyond project boundaries and captures the cost and benefits to society at large. In fact, such analysis is usually undertaken to ascertain whether an economic case exists for an investment decision. The economic cost/benefit analysis is also termed as the economic analysis of a project. Economic viability analysis includes an assessment of the economic benefits from, and the economic costs of, a project. The difference of these (benefits and costs as mentioned above) in present value terms, is the net economic benefit to society. Economic analysis is an integral part of project development studies and is normally undertaken before carrying out financial feasibility studies. |

|

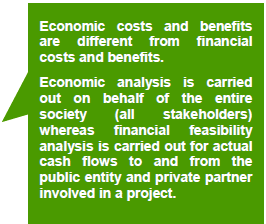

What distinguishes the economic viability analysis from a financial feasibility analysis is that economic viability analysis looks at the positive and negative effects of an investment decision that it might be difficult to attribute a market price to (such as the impact on indirect employment generation and economic activity, local environment and ecosystem, project affected people, etc.) and those that may not result in cash flows to the project.

| Differences between Financial Feasibility Analysis and Economic Analysis 1. The financial feasibility analysis involves direct costs and revenues associated with the project whereas an economic analysis takes into account the net benefit of the entire society. 2. The discount factor in financial feasibility analysis is WACC; in economic analysis, the discount factor is the social discount rate (economic opportunity cost of capital) 3. In financial analysis, some inputs may not have a financial cost and are therefore not shown in the analysis (e.g. if water at the intake is available to the water utility for free). However, the cost of these inputs would be shown in the economic benefit cost analysis if the input has a scarcity value (e.g., if raw water is diverted from another alternative use such as irrigation or hydropower). 4. Business cash flows may include accrued values, depreciation and other similar allowances. Benefit cost analysis does not use accruals, depreciation allowances or other non-cash items. 5. In benefit cost analysis, each cost and benefit is recognised fully at the time that it occurs (not accrued beforehand), timing is dealt through discounting the cash flow, and changes in the values of assets are dealt with by including residual asset values in the investment horizon. 6. In benefit-cost analysis, accounts receivable and payable are not recognised until the cash is actually received or paid. Working capital is not a cost, although the change in working capital during a particular period is either a cost or a benefit. Production costs are recognised fully at the time they occur. Changes in inventory may signal either costs or benefits, but the actual measurement of these is through production costs and sales. In brief, benefit-cost cash flows are very simple tables with everything recognised when it occurs. Source: "Capacity Development of National Capital Region Planning Board (NCRPB) Package 1 (Components A and C); Project Appraisal Manual April 2009, by ADB |

Reasons that necessitate economic analysis include the following;

1. Prevalent market prices of inputs and outputs may not represent/indicate their social value, viz. their social opportunity cost, because some markets are socially inefficient or do not exist at all: This would happen, for instance, in monopolistic or oligopolistic markets, where price includes a mark-up over marginal costs or in a situation where trade barriers exists that compel consumers to pay more than they would have paid elsewhere. Prices as they emerge from imperfect markets and from some public sector pricing or rationing policies may fail to reflect the opportunity cost of inputs.

2. Financial data, while important for budgetary reasons, may be misleading as welfare indicators: When market prices do not reflect the social opportunity cost of inputs and outputs, the usual approach is to convert them into accounting prices using appropriate conversion factors, if available, from the Planning Authority.

3. Certain project costs and benefits are without market values: For example, development of projects may have damaging repercussions on the environment, health and social well-being. This will require the Government to make additional investments to compensate for the damage. However, though this damage would not have a market price, it could significantly affect the success of the project.

Therefore, all direct and indirect effects of a project need to be assessed and quantified as costs and benefits for economic assessment. When market values are not available, such effects can be monetised through different techniques, in part depending on the nature of the effect considered. 'Money' valuation here has no financial implication.