3.3. Financing of PPPs

The output of the financial feasibility analysis is an assessment of whether the investors get their required returns. The key indicators that reflect financial viability include Net Present Value (NPV) and Internal Rate of Return (IRR).

| Financial Viability Assessment of a Project: When a project has: • A positive Net Present Value (NPV) of the project as a whole i.e., a project IRR exceeding the weighted average cost of capital • A positive NPV of the cash flow to the shareholder i.e., an equity IRR exceeding the cost of equity • Meets all debt service requirements It indicates that the project is financially viable. |

Typically, it is assessed whether the project is viable on its own - i.e., without any support from the public entity (financially free standing project).

| If a project is financially free standing, then it is analysed to see if the private partner could share some of the benefits with the public entities (typically in cash terms) and that could be the bidding parameter, all other things being addressed. The sharing of benefits is usually above an expected return by the private partner. For example, if the expectation of the equity investor is 22 per cent and the project generates an equity rate of return of 30 per cent, then it is expected that the private partner shares a return of 8 per cent (viz. 30 per cent minus 22 per cent). The same would also hold true for the support required for meeting equity return expectations. In other cases where the project is financially free standing, the public entity could also look for other options in that user charges could be reduced or the commitments of the public entity towards the project (in terms of share of obligations/risks) could be reduced. |

|

However, if the project is not financially free standing, multiple options need to be assessed to encourage private partner's participation in the project (i.e., ensuring that the benefits from the project meet the return expectations of the private sector). The returns estimate and the assumptions to be made for such an analysis are set out in Module 6 of the PPP Guide for Practitioners which sets out Financial Feasibility.

With regard to the financing of PPPs the following key questions need to be answered:

1. Are users willing and able to pay fees?

2. Is demand sufficiently stable or is demand very uncertain implying a need for alternative cost recovery schemes or guarantees?

3. Is demand sufficient for generating sufficient revenues to recover costs or is there a viability gap?

4. Is the private partner able to misuse possible monopolistic characteristics and generate excessive profits or is there a need for regulation?

5. If demand is more than expected will the private partner incur excessive profits or is there a need for regulation?

6. If necessary, how can the Government offer support e.g. Viability Gap Funding, guarantees, annuity payments, shadow toll?

When public entities want to make good decisions about whether to provide fiscal support for private infrastructure services, they need to be clear about the objectives they will be pursuing. Providing fiscal support for one service usually means providing less support to another particular service, or raising taxes, which means raising the cost of services generally. Therefore public entities need to have clear grounds for providing fiscal support.

The public entity needs to ask itself the following questions when considering providing public support to a particular private infrastructure project:

1. What objectives is the Government seeking to secure by providing fiscal support to the project?

2. Are current Government policies inhibiting the implementation of a satisfactory purely private project and, if so, could the Government achieve its objectives by changing those policies at no fiscal cost?

3. If not, what instruments of fiscal support does the Government have at its disposal?

4. How well does each instrument address the problem, taking into account problems of implementation as well as the desired effects? What is its expected benefit?

5. How much is each option likely to cost?

Given the assessment of the project not being financially viable with the defined scope and assumed PPP mode, the next challenge is to optimise the structure. There are several options to optimise the scope ranging from applying the Ministry of Finance, Government of India's Financial Support for PPPs in infrastructure, viz. VGF scheme or guarantees to scope changes. A well-structured financial model will be able to assess the impact of the different options on the NPV of PPP arrangements.

| One should also assess the impact of the different options on the risk profile of the PPP. It is obvious that using capital grant (under Financial Support for PPPs in infrastructure) will increase the NPV from a private sector perspective as it will reduce its financing. Extending the duration will also increase the NPV as it will add positive cash flows to the NPV calculation. Tariff increases may increase the NPV assuming that tariffs have not already been set at the profit maximising level. However tariff increases are also likely to increase the risk profile of the PPP. The way the users will react to higher tariffs and the elasticity would also have a bearing on the NPV. In this case the increased NPVs are not sufficient to offset the higher risk profile. |

|

| Reducing the scope may increase the NPV from a private sector perspective because the scope reduction may imply that costs will be reduced without a significant impact on the revenue potential. The scope reduction may also imply that the risk profile is reduced because it no longer includes, say for instance, the construction and maintenance risk of the excluded asset. In this case the consequence of the scope reduction is a financially viable project from a private sector perspective even through this may result in increased public sector risk exposure and a fiscal burden. |

|

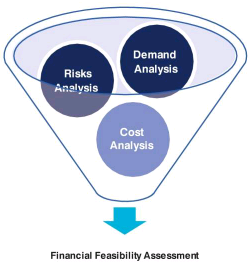

| Expanding the scope may increase the NPV e.g. advertisement rights that create additional revenues. However, the additional revenue stream may be very uncertain and consequently increase the risk profile. In such an event, the increased risk profile outweighs the increased NPV potential. The following questions are typically answered in conjunction with the value drivers of the project: 1. Demand (which translates into revenues or other benefits to the project) 2. Risks (across the spectrum of project development, implementation and operations) 3. Costs (capital and operating expenditures) |

|