Note on discount rate assumption

The discount rate is utilised as a way of calculating the net present value ("NPV") of future cashflows, and the selection of an appropriate rate is crucial to informing the Government Entity's decision, as a result of which it must be done only following extensive analysis and consultation. Globally, there are a number of approaches to calculating a suitable discount rate, ranging from a long-term government borrowing rate, to a government rate plus a Risk Premium applied to the PPP model, to the cost of capital of the private sector party. Due to the mechanics of how a discount rate calculation works, a higher discount rate would increase the likelihood of a PPP passing the VfM test.

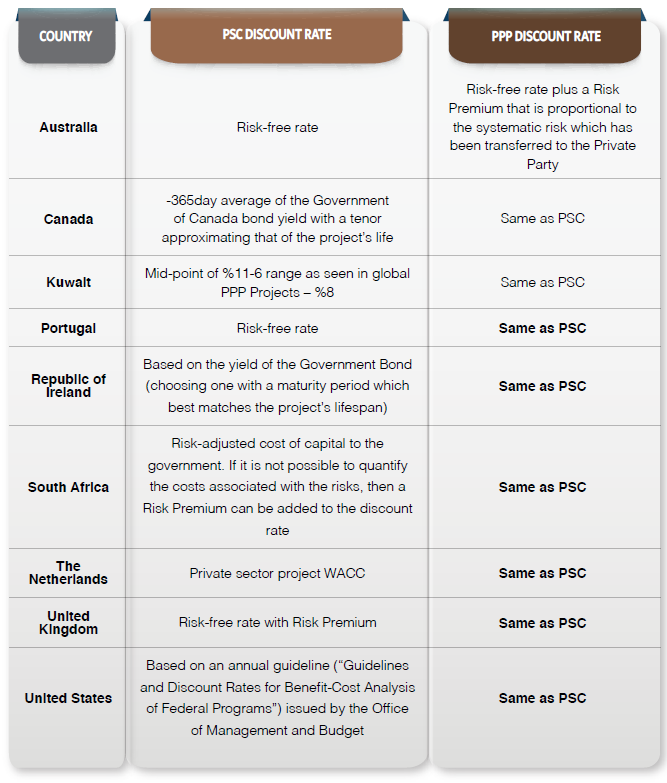

Attached below is a table benchmarking the discount rates utilised as part of the PSC and PPP models around the world:

|

Figure 15: Benchmarking analysis of discount rates utilised as part of the PSC and PPP models in different countries |

In summary, there are three broad options for determining the discount rate:

1. Where the risk-free rate is utilised for the PSC and PPP - as in Portugal, for example;

2. Where the risk-free rate with a project Risk Premium is utilised for the PSC and PPP - as in the United Kingdom, for example; and,

3. Where the risk-free rate is utilised for the PSC and the risk-free rate plus a project Risk Premium is used for the PPP - as in Australia.

Option 1: The government risk-free rate - usually a government bond with a tenor that is similar to the project length - is used for the PSC and the PPP models.

PSC model - as the government will borrow as a whole, and not on particular projects, in Dubai, it is appropriate to use the risk-free rate; and,

PSC model - as the government will borrow as a whole, and not on particular projects, in Dubai, it is appropriate to use the risk-free rate; and,

PPP model - using the same rate allows for a like-for-like comparison for the evaluation of VfM.

Option 2: Sum of the government risk-free rate plus a project Risk Premium is utilised for both the PSC and the PPP models with the purpose of reflecting the project cost of financing for the private sector accurately and incentivising the private sector to participate in riskier projects. The PPP Project Team must note that, for the same project, everything else staying equal, using this higher discount rate is likely to show greater Value for Money than using only the risk-free rate, as shown below.

| NPV is the sum of the present values of future cash flows. The formula for calculation is shown below:

Where UC is the unitary charge/availability payment, r is the discount rate, and the concession period is 25 years. If the discount rate is higher, the denominator in the above equation becomes bigger. Hence, the NPV becomes smaller. As payments in the PPP model are over the whole project term, the benefit of discounting are more apparent in a PPP model than in a traditional procurement model, wherein the payment for construction is done during the construction period only. |

Option 3: which is only followed in Australia, the PSC model uses the risk-free rate, whilst the PPP model uses the risk-free rate plus a project Risk Premium. After calculating the project Risk Premium using an asset beta and a market Risk Premium, the systematic risks are listed out to calculate the portion of the Risk Premium transferred to the private sector. While this method is novel, there are some issues with it, particularly in a Dubai context, as deriving an asset beta and a subsequent project Risk Premium is conditional on a liquid equity market, which is not the case regionally.

In general, for Dubai, we would recommend Option 1. If the tenor of Dirham-denominated bonds might not always match the requisite concession period, premium yield adjustments taking account of the USD-denominated international bonds and interpolation should be applied to arrive at a final discount rate. However, over time, as the PPP market becomes more liquid and Dubai extends the yield curve with regular debt issuances, it is recommended that the PPP Project Team consider moving to Option 2 - wherein the risk-free rate plus a Risk Premium is utilised as the rate for the PSC and for the PPP.