The wider costs of Carillion's collapse

3.21 In June 2018 we reported that the costs to the government of Carillion's liquidation would be £148 million. This was the cost to the Cabinet Office of ensuring that the Official Receiver could continue Carillion's service contracts without disruption until new arrangements could be made.

3.22 The Official Receiver, HM Treasury and the Cabinet Office have worked together since January 2018 to collect money owed to Carillion. As a result, the Cabinet Office now expects to be repaid some of its loan, and at the time of this report's preparation its expected loss was £62 million.16 This does not include the additional costs to the public sector due to the delays in the two hospital construction contracts covered by this report.

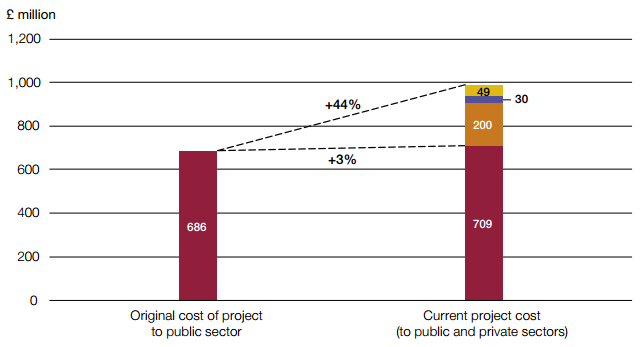

| Figure 7 The current expected cost at Midland Metropolitan The total cost of the project to build and operate the hospital for 30 years is expected to have increased by 44% but the cost to the taxpayer is expected to have increased by only 3%

The increased build cost to the public sector is largely offset by losses borne by the private sector

Notes 1 The 'current' costs represent the Sandwell and West Birmingham Hospitals NHS Trust ('the Trust's') estimate at the start of December 2019. 'Original' costs are based on the PFI contract and the Trust's estimate of other costs under the original plan. We have not independently verified these estimates. Where costs are contractually linked to the Retail Price Index (RPI) they have been estimated using the Office for Budget Responsibility's forecast (published March 2019). All costs have been expressed in 2018-19 terms using Gross Domestic Product (GDP) Deflators (published June 2019) to ensure comparability. The last line shows the same costs discounted at the government's discount rate of 3.5%. 2 The 'PFI-financed contribution from private sector' includes construction costs, other costs of the PFI company, and fees and interest on private finance during construction that were included in the PFI contract. This includes the value of the construction work completed by Carillion which was assessed as £212 million. We have assumed that costs were incurred by the PFI company in line with the PFI contract until the contract was terminated. IUK contributed £3 million which we have included in the 'public sector contribution' rather than this line. 3 We have estimated construction overspend in Carillion and its supply chain using losses it reported in 2017 (adjusted for inflation). This is based on incomplete information about the extent of Carillion's losses. Carillion's subcontractors may also have incurred losses. 4 All construction costs exclude VAT. The Trust expects to pay £68 million VAT on completing construction. The Trust and HMRC do not currently agree on the VAT treatment. The £315 million figure includes the Balfour Beatty construction contract and other costs. 5 The 'Interest on private finance and other costs included in the PFI unitary charge' is calculated as the total unitary charge less the costs of construction (including fees and costs of the PFI company), facilities management, and maintenance costs over the 30-year contract. 6 Total losses borne by the private sector have been estimated at £279 million (adjusted for inflation) based on the information available and assuming that the planned investment in the PFI contract was made and will not be recovered. This information is not complete, for example we do not know the extent of losses in the supply chain, whether there will be any amounts recovered from the liquidation of the PFI company, or the extent to which losses were reduced or passed from the original investors to other organisations via fees paid during construction (for example, IUK Investments Ltd and Dukehill Investments Ltd paid Carillion a premium of £1.1 million and £287,000 when they bought their shares), or risk management activities such as insurance or securitisation. 7 The £3 million invested by IUK Investments Ltd who owned 10% of the PFI company is included in the cost to the public sector. Source: National Audit Office analysis of the PFI model and financial information from the Trust | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Cost to public sector

Cost to public sector Loses reported by Carillion Construction in 2017

Loses reported by Carillion Construction in 2017 Losses borne by private sector investors in the

Losses borne by private sector investors in the  Losses borne by providers of letter of credit to the

Losses borne by providers of letter of credit to the

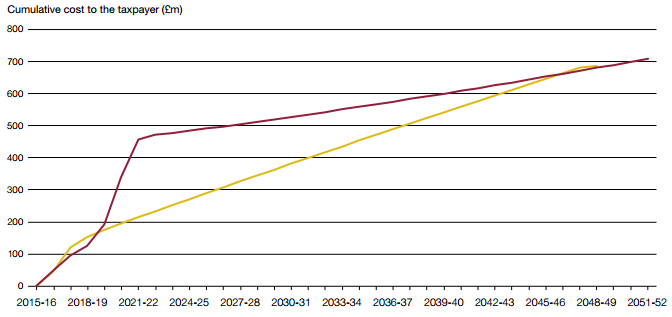

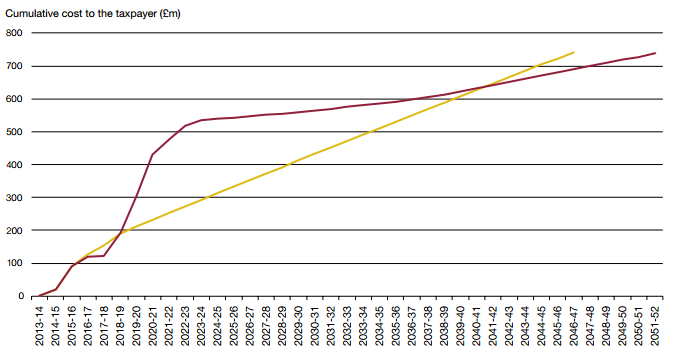

| Figure 8 The expected cost to the taxpayer of Midland Metropolitan over time Under public funding, the expected real-terms cost to the taxpayer to build and operate Midland Metropolitan has increased by only 3%, to £709 million, but more of the costs are incurred earlier

Source: National Audit Office analysis of the PFI model and financial information from the Trust |

Current expected cost to taxpayer

Current expected cost to taxpayer Original expected cost to taxpayer under

Original expected cost to taxpayer under

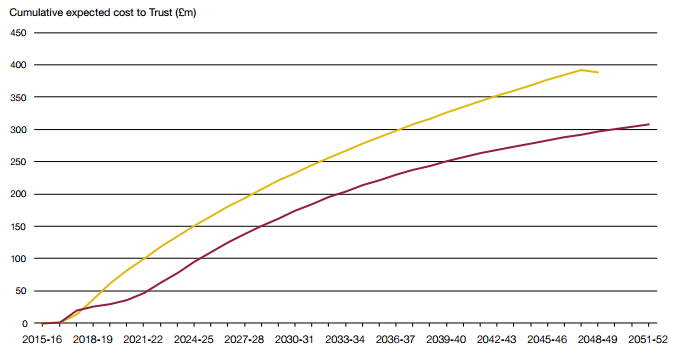

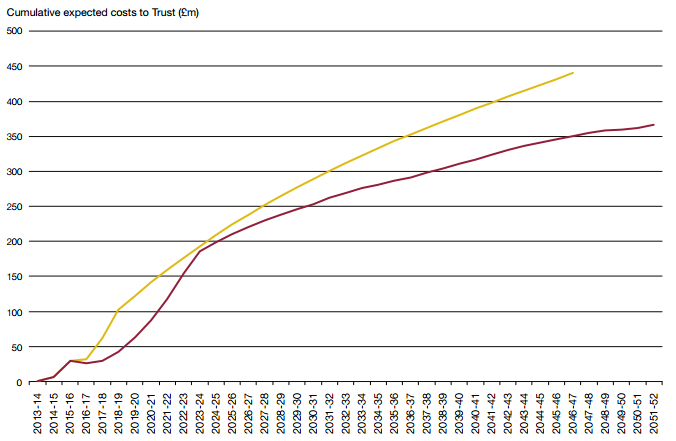

| Figure 9 The expected cost to the Trust of Midland Metropolitan over time The Department of Health & Social Care and NHS England and NHS Improvement (NHSE&I) are paying for the front-loading of the project costs so the Trusts are currently expected to be financially better off overall than if the PFI contracts had gone ahead as originally planned. The Sandwell Trust is now expected to pay an estimated £308 million in total, a reduction of £81 million

Notes 1 Shows the cumulative expected costs, in 2018-19 terms (see Figure 7), to the Sandwell and West Birmingham Hospitals NHS Trust ('the Sandwell Trust') over 30 years under the original PFI arrangement and under the current forecast. 2 The graph shows an estimate of the cash cost (in 2018-19 terms) to the Trust based on the expected accounting treatment of the original and current forecasts from Figure 7, net of funding mechanisms such as receipt of Public Dividend Capital (PDC) and including intra-government payments such as VAT and the PDC dividend. We have not modelled the impact of income generated by the hospital or changes to the value of the hospital building from revaluation or impairment as these are not yet known. The expected PDC dividend paid has been estimated at 3.5% of the average impact on net assets. The results have then been converted to 2018-19 terms in the same way as in Figure 7. Source: National Audit Office analysis of the PFI model and financial information from the Trust |

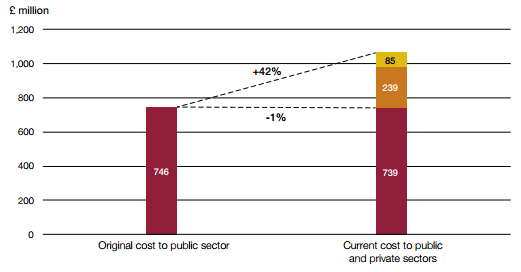

| Figure 10 The current expected cost at Royal Liverpool The total cost of the project to build and operate the hospital for 30 years is expected to have increased by 42% but the cost to the taxpayer is expected to have decreased by 1%

The increased build cost to the public sector is offset by losses borne by the private sector

Notes 1 The 'current' costs are the Royal Liverpool and Broadgreen University Hospitals NHS Trust's ('the Trust's') latest estimate. 'Original' costs are based on the PFI model and the Trust's estimate of other costs under the original plan. We have not independently verified these estimates. Where costs are contractually linked to the Retail Price Index (RPI) they have been estimated using the Office for Budget Responsibility's forecast (published March 2019). All costs have been expressed in 2018-19 terms using Gross Domestic Product (GDP) Deflators (published June 2019) to ensure comparability. The last line shows the same costs discounted at the Green Book discount rate of 3.5%. 2 The 'PFI-financed contribution from private sector' includes construction costs, other costs of the PFI company, and fees and interest on private finance during construction that were included in the PFI contract. This includes the value of the construction work completed by Carillion which was assessed as £269 million. We have assumed that costs were incurred by the PFI company in line with the PFI contract until the contract was terminated. 3 We have estimated construction overspend in Carillion and its supply chain using losses it reported in 2017 (adjusted for inflation). This is based on incomplete information about the extent of Carillion's losses. Carillion's subcontractors may also have incurred losses. 4 All construction costs exclude VAT. The Trust expects to pay £75 million VAT on completing construction and on some of the other costs it will incur. The Trust and HMRC do not currently agree on the VAT treatment. 5 Because the Trust has not re-forecast the cost of maintaining the hospital we have based this line on costs in the PFI model, adjusted for the delay to the hospital opening. 6 The 'Interest on private finance and other costs included in the PFI unitary charge' is calculated as the total unitary charge less the costs of construction (including fees and costs of the PFI company), facilities management, and maintenance costs over the 30-year contract. 7 The retail concession would have provided the PFI investors with additional income, which will now accrue to the public sector. 8 The public sector paid £42 million to the private sector lenders to terminate the contract. This is now shown in the righthand column as it is not a net increase to the cost of the project. 9 Phases 2 and 3 of the project will see the original hospital demolished and the site used to provide an underground carpark and public plaza. 10 Total losses borne by the private sector have been estimated at £324 million (adjusted for inflation) based on the information available. This assumes that the planned investment in the PFI contract was made and will not be recovered, and is net of the £42 million payment to terminate the PFI contract. This information is not complete, for example we do not know the extent of losses in the supply chain, whether there will be any amounts recovered from the liquidation of the PFI company, or the extent to which losses were reduced or passed from the original investors to other organisations via fees paid during construction or risk management activities such as insurance or securitisation. Source: National Audit Office analysis of the PFI model and financial information from the Trust | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Figure 11 The expected cost to the taxpayer of Royal Liverpool over time Under public funding, in real terms the expected cost to the taxpayer to build and operate Royal Liverpool has decreased by 1% to £739 million, but more of the costs will be incurred earlier

Source: National Audit Office analysis of the PFI model and financial information from the Trust |

| Figure 12 The expected cost to the Trust of Royal Liverpool over time The Department of Health & Social Care and NHS England and NHS Improvement (NHSE&I) are paying for the front-loading of the project costs so the Trusts are currently expected to be financially better off overall than if the PFI contracts had gone ahead as originally planned. The Liverpool Trust is expected to pay an estimated £366 million in total, a reduction of £74 million

Notes 1 Shows cumulative costs in 2018-19 terms to the Liverpool University Hospitals NHS Foundation Trust (the Liverpool Trust) over 30 years under the original PFI arrangement and under the current forecast. 2 The forecast includes an estimate of the cash cost (in 2018-19 terms) to the Trust based on the expected accounting treatment of the original and current forecasts from Figure 10, net of funding mechanisms such as receipt of Public Dividend Capital (PDC) and including intra-government payments such as VAT and the PDC dividend. We have not modelled the impact of income generated by the hospital or changes to the value of the hospital building from revaluation or impairment as these are not yet known. The expected PDC dividend to be paid has been estimated at 3.5% of the average impact on the Trust's net assets. The results have then been converted to 2018-19 terms in the same way as in Figure 10. Source: National Audit Office analysis of the PFI model and financial information from the Trust |

______________________________________________________________________________

16 Letter from the Insolvency Service to the House of Commons Business, Energy and Industrial Strategy Committee, 30 September 2019.