Capital funding sources

3.2 NHS providers receive payments for providing care to patients. These payments include a consideration for costs to cover the wear and tear of assets. Those providers that can, on aggregate, deliver patient care at or below the cost they receive for it can more easily use these internally generated funds for replacing and maintaining their assets. For many NHS providers, internally generated funds do not support their total capital spending plans. Consequently, they must look for additional sources of funding. Capital funding sources include the following:

• Internally generated funds and use of surpluses (paragraphs 3.2 and 3.3).

• Selling land (paragraph 3.4).

• Loans from the government, as well as capital funding for strategic central programmes (paragraph 3.6).

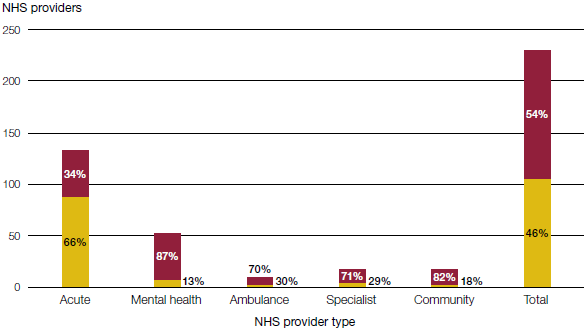

3.3 In 2018-19, 124 out of 230 (54% of NHS providers) delivered a surplus (Figure 12). Delivering a surplus improves the NHS providers' cash balance. Those in surplus, particularly NHS foundation trusts, have specific freedoms to use their surplus for capital spending or to let the surplus carry forward into the following year. NHS providers in deficit have scarce cash resources and have no means of accessing cash from surpluses elsewhere in the NHS, such as from within their sustainability and transformation partnership (STP), and must resort to seeking loans from the Department of Health & Social Care (the Department) to fund agreed capital spending plans. The current capital regime means that the availability of cash does not necessarily match where there are the most urgent capital needs. The greatest number and proportion of NHS providers in deficit were in the acute sector (in other words, general hospital services).

| Figure 12 While 54% of all NHS providers broke even or produced a surplus in 2018-19, this falls to 34% of acute providers |

|

|

|

|

| Source: NHS Improvement, Consolidated NHS provider accounts 2018-19, HC 2376, July 2019 |

Number of providers breaking even/in surplus

Number of providers breaking even/in surplus Number of providers reporting deficit before impairments and transfers

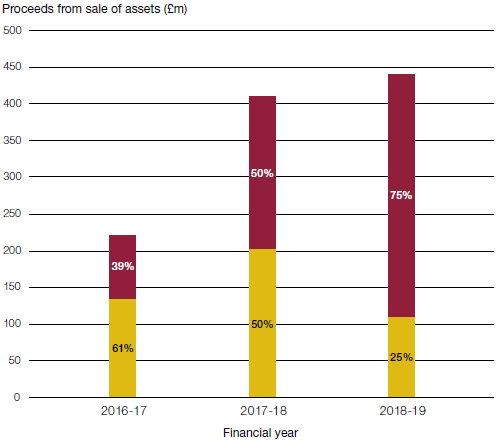

Number of providers reporting deficit before impairments and transfers3.4 NHS providers can sell assets to raise funds. Government policy encourages public sector entities to sell assets where they no longer serve a public purpose. HM Treasury guidance has specific rules about the use of sale proceeds, and how they should be split between capital and revenue budgets. Typically, once sold, the value of the asset in the NHS providers' accounts is available for capital investment, and profits are available for day-to-day spending, although the level of profit that benefits day-to-day spending is limited and monitored. Figure 13 overleaf shows that the overall proceeds from asset sales increased by 99% between 2016-17 and 2018-19, from £222 million to £441 million (annual increases of 84% between 2016-17 and 2017-18, and 8% between 2017-18 and 2018-19). The proportion of profit made on asset disposal also increased from 2016-17 to 2018-19 by 36 percentage points (from 39% in 2016-17 to 75% in 2018-19). This assists the revenue position and meant that not all these asset proceeds have been available to reinvest into capital.7 The high value of land in London creates a potentially large source of funding for London's NHS providers.

| Figure 13 Proportionately the profit made on sale of assets by NHS trusts and NHS foundation trusts (NHS providers) has increased by 36 percentage points |

|

|

|

|

| Source: National Audit Office analysis of Consolidated NHS provider accounts |

3.5 A reduction in an asset's value due to, for example, damage sustained, a decline in market value or change in use, is known as an impairment. For the Department, which includes NHS providers, impairments stood at around £1.6 billion during the period 2013-2015. In the following two years there was a noticeable increase in impairments: £2.2 billion (2015-16) and £2.6 billion (2016-17). In January 2016, NHS providers were guided by NHS Improvement to "review all equipment and buildings asset lives given that less capital will be available for replacement in future". This guidance encouraged NHS providers to apply an alternate method of valuation "where advantageous", which would result in a reduction in an asset's value, thus creating a one-off impairment, and therefore a reduction in depreciation charges. Creating the one-off impairment does not hinder the financial performance figure that is used by NHS Improvement to hold NHS providers to account, and a reduction in the depreciation charge improves the 'bottom line'. Reducing the book value of assets can also contribute to improving a trust's bottom line by reducing its annual dividend payment to the Department.

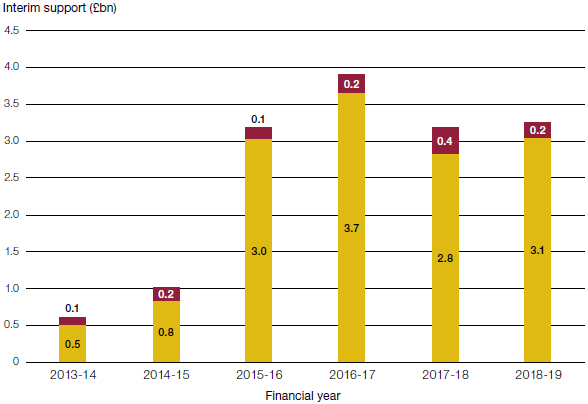

3.6 Since the period 2013-15, there has been an increase in the interim financial support from the Department to NHS providers. This interim support is for NHS providers in financial distress to support the continued delivery of services (Figure 14). The number of providers receiving interim capital support has also grown, with 35 NHS providers receiving support in 2018-19 compared with 17 in 2013-14. In 2018-19, the combined debt for capital and revenue interim borrowing reached £10.9 billion.

3.7 In 2018-19, £3.6 billion of the Department's capital limit was for NHS providers, but NHS providers spent £3.9 billion. The overspend of £377 million was balanced by underspends elsewhere in the Department. NHS providers generated 76% (£3 billion) of the total capital expenditure from internally generated funds, loans and asset disposals. The Department and NHS England and NHS Improvement (NHSE&I) provided £543 million (14% of NHS providers' capital expenditure) in the normal course of business for strategic projects, with, for example, £141 million for emergency and urgent winter preparations. The remainder is made up of other capital support (6%) and Private Finance Initiative residual interest (4%).

| Figure 14 Since the period 2013-2015, NHS providers have received increased support from the Department |

|

|

|

|

| Note 1 Interim revenue and capital support drawn in-year by NHS providers as loans or public dividend capital. |

| Source: National Audit Office analysis of information extracted from the Department of Health & Social Care Section 40 publications |

_____________________________________________________________________________________________

7 The National Audit Office report on government's land disposals (Comptroller and Auditor General, Investigation into the government's land disposals and strategy, Session 2017–2019, HC 2138, National Audit Office, May 2019), said that: "It would be a concern if departments are selling land and property to support day-to-day running costs, rather than to invest in refurbishing existing assets or purchasing new ones."