Real Options Analysis

A5.17 A 'real option' is a choice that becomes available through an action or an investment opportunity. Real options analysis recognises information about uncertainty can change over time through research and learning, and initial decisions can be changed as a result. If the value of this flexibility is not accounted for, the social value of an option will be systematically underestimated.

A5.18 Real options analysis is particularly applicable to proposals that exhibit significant uncertainty following initial investment, but where learning opportunities and flexibility in future decisions can help mitigate this. It is most useful where knowledge that is relevant to the choice of options is growing. If there is limited flexibility in the future, the benefits of new information are unlikely to be realised.

A5.19 Decisions should be taken with the best available information, recognising that this may change in future and flexibility to respond should not be used to justify delay. In addition to considering the range of options available, describing how information is likely to be acquired through monitoring and evaluation should be incorporated into appraisal. In practice, a decision will only have value if it can be enforced. The length of time before exercising a decision will also affect its value. The greater the time for useful information to become available, the greater the scope for the value of a decision to vary.

A5.20 An example of real options analysis can be found in Box 23 below.

Box 23. Example of Real Options Analysis

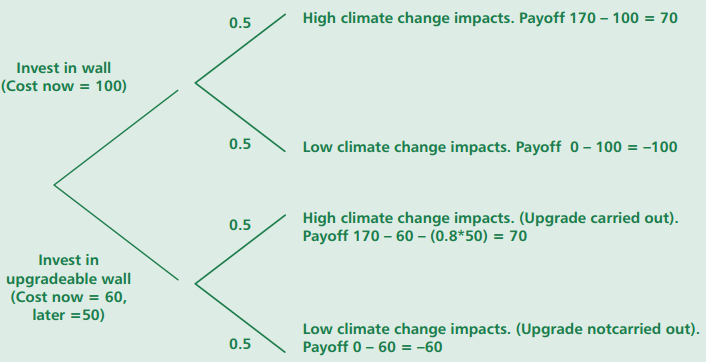

Case Study: Appraisal using a real options approach Consider a proposal for investing in infrastructure protecting against the impacts of river flooding due to climate change. Because of time required to build the infrastructure, this is best done in advance but there is uncertainty about future impacts. There are two options: invest in a wall, or invest in groundworks for a wall which has the option to be fully upgraded quickly in the future. There is an equal probability of high or low climate change impacts in the future. The standard wall costs 100, and has benefits of 170 from avoided flooding if high climate change impacts occur (zero otherwise). The groundworks for the upgradeable wall cost 60, the future upgrade costs 50 and the benefit is also 170 if high climate change impacts occur. The upgrade can however be put off until there is more certainty about climate change. The information can be set out in a decision tree:

Simplifying assumptions: residual damages under the "do not invest" strategies have been ignored; the discount factor for the future decision to upgrade or not is 0.8. The expected value of investing in the standard wall is a simple net present calculation, calculating the expected costs and benefits of the investment. The NPV is (0.5*70) + (0.5*-100) = -15. This suggests the investment should not proceed. Flexibility over the investment decision allows the possibility to upgrade in the future if the impacts of climate change are observed to be high. The expected value of this option can be calculated. If the impacts of climate change turn out to be high enough to warrant upgrading, then the value of the investment is 70 in net present value terms. If the impacts are low, no upgrade is carried out but the earlier groundworks are sunk costs, totalling 60. However, these sunk costs are lower than in the case of the "standard" wall and overall, the expected value of investing now with the option to upgrade in the future is (0.5*70) + (0.5*-60) = +5. Comparing the two approaches shows an NPV of -15 for the standard approach, and +5 for the Real Options approach. The Real Options approach also has an unmonetised benefit in allowing better views of the river for longer. Flexibility to upgrade in the future is reflected in the higher NPV, and switches the investment decision. Source: Department for Environment, Food and Rural Affairs |