CHAPTER 3 Mechanisms Facilitating Return on Private Investments in PPP Projects

This chapter focuses on the primary forms of payment mechanisms used to finance PPPs. The essential characteristics of models are described in order to estimate their respective advantages and disadvantages. The comparison reveals areas where each mechanism might be the most efficient. The research findings show that the most popular mechanisms are public and users' payments. The criterion for classification is the source of remuneration. The selected examples of finance mechanisms are demonstrated at the end of the chapter.

|

Box 2. Project Bond Initiative Project Bond initiative (PBI) was developed by the European Commission and the European Investment Bank (EIB) as a means of encouraging new financial instruments to make infrastructure projects more attractive to investors. The PBI aims to promote the development of capital markets for financing European infrastructure projects for transport, energy and information technology and communication. Institutional investors have a high potential to invest in large-scale infrastructure projects through the capital markets. Thus, project bonds are an alternative source to bank loans and public financing. The PBI intends to reduce the dominance of commercial banks in infrastructure financing in Europe, and promote the contribution of alternative investors. Project bonds are not a new phenomenon; they have been used for financing projects in the USA, Canada and Asia for more than 15 years. Although project bond financing has always played a minimal role in project finance globally, its importance is increasing. The first financing operation in Germany with EU project bonds closed in late August 2014. The project A7 concerns the extension of the motorway between the Bordesholm junction in Schleswig-Holstein and the Hamburg Nordwest junction. During the construction period, traffic will keep on flowing. The project company is paid based on availability payments. The total financing is up to €770 million. The duration of the concession is 30 years. The EIB is providing a subordinated loan of around €90 million for the project, representing about 20% of the volume of the senior debt through the issuance of capital market instruments. The bond investors were EIB, AXA, KfW IPEX, MassMutual, Aegon, ING and Sun Life. The pilot phase of the PBI plays a significant role in the future of the initiative. Overall, the pilot experiences have proved that project bonds may be a working instrument to finance infrastructure facilities. Institutional investors such as pension funds and insurance companies have shown their interest given that project bonds can perfectly match long-term liabilities with long-term assets and increase their yields. Source: Journals.vgtu.lt Ideas for Policy-Making • Introduce the system for comprehensive demand risk assessment as a way of promoting the efficiency of PPPs that rely on user payments • Implement mechanisms, facilitating return on private partner's investment, focusing on all vital aspects of the PPP project • Create assessment tools for calculation of the sufficient volume of MRG, appropriate for public and private partners

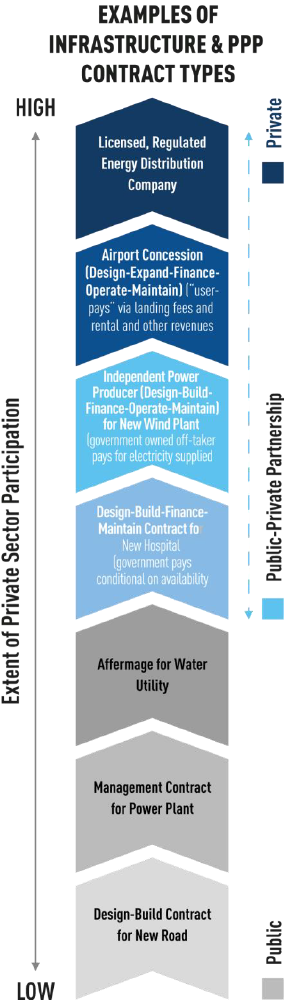

| Choice of Payment Mechanisms Depends on Demand Risk Management Payment mechanisms define how the private party is remunerated.i Generally, PPP payment mechanisms, as the principal means for allocating risks and providing incentives, can be divided into two groups, focusing on the source of income - from public partner or users. The two primary forms of payment mechanisms in PPPs include availability payment when costs of the private partner are covered from the budget and revenue-based user payments when the private partner's income stems from commercial activities. The Survey has shown that both of them are used in all G20 countries. The choice of the payment mechanism for a particular PPP project is a form of risk transfer because the payment mechanism allocates "demand risk" - risk that the infrastructure asset does not generate enough user fees to pay for its design, construction and maintenance.ii Since the 1980s, the availability payment mechanism has become prominent in the United Kingdom, Canada and Australia, as these countries executed PPPs for social facilities, such as hospitals and schools. According to the Survey, availability payment is among the most common payment mechanisms. Majority of PPP projects in Canada use the availability payment mechanism, regardless of whether the asset can generate sustainable revenue. An availability payment mechanism means that public partner makes recurring payments to a private one for making the PPP asset available for useiii, regardless of whether the public partner uses the PPP asset. In order to receive payment, the private partner must ensure that the asset meets specific performance standards and is "available" for use by the public. With an availability payment mechanism, the public partner covers the demand risk for the PPP project.iv It is widely used in social infrastructure, where demand- side risks are usually high. Additionally, in some transport sub-sectors, this practice is becoming increasingly common (toll-free roads, rail, and water transportation).v The natural structure of a PPP payment mechanism is unitary, as the public partner is paying for services, and if there is no service, there should be no payment. By using the availability payment mechanism, the public partner can limit the profit of the private partner.vi The private partner collects user charges directly from users to recoup project implementation costs. Such revenue regime is simplified for public partners due to the practically neutral budgetary impact of such projects. By charging users, the approach of setting and adjusting tariffs becomes a vital risk allocation mechanism. In some PPPs, the private party may set tariffs and the tariff structure at its discretion. However, in many countries, user-pays PPPs are implemented in monopolistic sectors, and tariffs are typically regulated by the government (along with service standards), to protect users. The demand risk is on the private partner, but it also allows for a potentially higher profit. At the same time, demand risks can be hard to estimate. Many factors may affect the continued use of a toll road, for example, the significant deviation in mass transit, fluctuation of fuel prices and the relocation of people from a particular areavii. Thus, it often can be hard to reach a return on investment without any public support, which leads to the use of mixed payment models where public and private partners share risks of demand. The mechanism of minimum revenue guarantee (MRG) is a common practice in several countries, such as Brazil, Russia and Turkey, which allows for sharing the risks of project profitability between parties. In the face of significant revenue risk in PPPs, MRG is an instrument that can be used by governments in order to attract private investors.viii By offering MRG, the public partner agrees to mitigate the revenue risk taken by the private sector. However, the practice of legal regulation of MRG in countries evidences different approaches to the conditions for compensation to the private partner. MRG appeals to governments due to its ability to induce more private investment without any immediate increase in reported government spending or debt.ix However, PPP practices indicate that public partners are not always sure of the thresholds of guarantees that should be offered, which sometimes leads to over-guarantees.x MRG is a valuable instrument to enhance private partners' confidence through public partner's commitment. However, it may give rise to significant challenges to long-term fiscal management. The process of evaluating and designing MRG is comprehensive and requires transparency in accounting, reporting and budgeting. Australia In Australia, the National PPP Policy and Guidelines outline the broad commercial principles that jurisdictions apply to manage PPP financing. As these principles are a high level guide, each jurisdiction has developed supplementary policies and guidance to manage PPP financing consistent with the national principles. In the Australian Capital Territory, the availability payment is calculated monthly with abatements (deductions from payments) based on "unavailability' of the required services. Performance abatements typically only apply after the expiry of a rectification period and for performance failures above a monthly threshold. The abatements are applied in constructions, transportation, road projects, BOOT and output-based projects. In the Northern Territory, availability payments have been used to facilitate PPP projects. Options for user charges and other concession arrangements may have more limited applicability in the Northern Territory due to its small and widely dispersed population. In New South Wales, the Government pays the project company in return for making the assets available for use. For specific availability PPPs, the Government will make capital contributions during construction, in order to reduce the private financing requirements. The capital contributions are typically linked to the achievement of KPIs. Queensland has adopted availability payment mechanisms in PPP procurement to achieve optimal risk allocation and correct incentives to the private proponent. The appropriateness of a payment mechanism in achieving quality service outcomes is considered on a project-by-project basis. In Victoria, the private party is paid for making the facility available to specified standards over the contract term, especially in social infrastructure. Abatements are applied for any availability and quality failures (when key performance indicators are not met), or the private party is paid through the collection of toll revenue over the contract term. In Western Australia, both availability payments and user payments have been used as appropriate. The Republic of Korea With a 15-year experience in PPP program, the Republic of Korea has an established institutional framework and mature PPP market. The financial crisis that hit the Republic of Korea in late 1997 was a drag on the growth of the PPP projects.xi In 1998, the government introduced the «Act on Private Participation in Infrastructure», which called for reinvigorating PPPs through various government measures, including the introduction of minimum revenue guarantee. The Republic of Korea modified this law in January 2005, expanding the range of facilities covered from economic infrastructures, such as transport facilities - roads, railways, seaports, and environmental facilities - to social infrastructures, such as schools, military residences, housing and welfare facilities for the aged, and cultural facilities. In October 2009, the minimum revenue guarantee was abolished and replaced by another government support measure - compensation of base cost -where the government shares investment risk within the set limit.xii |

References

i "The Guide to Guidance How to Prepare, Procure and Deliver PPP Projects." Last modified August 6, 2019. https://www.eib.org/attachments/epec/epec_the_guide_to_guidance_en.pdf?f=search&media=search.

ii "Payment Mechanism: The First Form of Risk Transfer in Public-Private Partnerships." Last modified August 6, 2019. https://www.aon.com/attachments/risk-services/AIS_Payment-Mechanism-White-Paper.pdf.

iii "An Evaluation of Availability-Based Payments for US Public-Private Partnerships" Last modified August 6, 2019. http://www.academicstar.us/UploadFile/Picture/2017-8/2017813223028544.pdf.

iv "Payment Mechanism: The First Form of Risk Transfer in Public-Private Partnerships" Last modified August 6, 2019. https://www.aon.com/attachments/risk-services/AIS_Payment-Mechanism-White-Paper.pdf.

v "Availability Payments." Last modified August 6, 2019. https://ppp-certification.com/ppp-certification-guide/410-availability-payments.

vi "What Are Payment Mechanisms?" Last modified August 6, 2019. https://www.swg.com/insight/ppp-resources/what-are-payment-mechanisms/.

vii "George Nwangwu. "Managing Traffic Demand Risk in Road Sector Public-Private Partnerships (PPPs) through the Use of Put and Call Option Agreement." Vol.8, No.22, 2017 (n.d.). https://pdfs.semanticscholar.org/21c3/6a80dd4669c7870c5690ec39016739faa87f.pdf.

viii "Ting , Liu. "Minimum Revenue Guarantee Creates Value, but It's Not a Free Lunch." April28, 2016, August 6, 2019. https://gpc.stanford.edu/gpcthinks/minimum- revenue-guarantee-creates-value-its-not-free-lunch.

ix "Minimum Revenue Guarantee." Last modified August 6, 2019. http://www.ppp-infrastructure.com/minimum-revenue-guarantee/.

x Xu, Y., J. F. Yeung & S. Jiang . Determining Appropriate Government Guarantees for Concession Contract: Lessons Learned from 10 PPP Projects in China. International Journal of Strategic Property Management, 2014.

xiJay-Hyung Kim, Jungwook Kim, Sunghwan Shin, Seung-yeon Lee. Public-Private Partnership Infrastructure Projects: Case Studies from the Republic of Korea, 2019. https://library.pppknowledgelab.org/documents/2251?ref_site=ppiaf&country%5B%5D=Korea%2C%20Rep.&restrict_documents=false&restrict_pages=true&site_source%5B%5D=PPIAF.

xiiPublic-Private Partnership Infrastructure Projects: Case Studies from the Republic of Korea, 2019. https://www.adb.org/sites/default/files/publication/29032/ppp-kor-v1.pdf.