Review documents - Development of the PSC

In considering the development of the PSC in the DBC, we focussed on the two items specified in the IR scope as to whether the budget in the DBC:

• Was based on a reasonable supporting analysis and assessments of costs; and

• Had appreciation of inherent and contingent risks.

Budget in the business case supported by a reasonable analysis and assessments of costs

To assess the work done during the PPP DBC stage regarding PSC cost lines, we firstly had regard to the following definition of the PSC available at that time (i.e. sourced from the 2009 New Zealand PPP Guidelines).

"... The PSC is a measure of what the project would cost if delivered through conventional procurement. The PSC is made up of: • the construction and operating costs of a project, plus • provision for competitive neutrality adjustments to remove any advantages or disadvantages that accrue to a public sector procurer by virtue of its public ownership, plus • provision for any additional costs and risks that would be transferred to the private sector partner under a PPP. These risks need to be added as a cost to the PSC because the public sector party would bear the cost of any risks that occur under conventional procurement... " Source: Guidance for Public Private Partnerships (PPPs) in New Zealand: NZ Treasury, October 2009 V1.1, page 14. |

Note, the above 2009 definition of the PSC is essentially similar to the following slightly more expanded definition provided on page 2 of the 2015 version of the New Zealand PPP guidelines, i.e., "...The PSC is an estimate of the risk adjusted whole of life cost of a project if it were to be delivered by the procuring entity using conventional procurement methods...". We note that the 2009 PPP Guidelines available to the Project Team during development of the PSC only provide a very high-level summary of the PSC and how it is developed. However, those 2009 PPP Guidelines explain to readers that the Australian National PPP Guidelines (i.e. Volume 4: Public Sector Comparator Guidance) is a useful guide for putting together the PSC.

For the purpose of this part of the IR, we use the whole-of-life costing components comprising TGP's construction and operating cost estimates as the main definitional element of the PSC. We noted from the review documents that an assessment was prepared of the competitive neutrality adjustment, but we did not explore this cost line in any detail as it forms part of the value for money assessment (which is outside of the IR scope). For risks transferred to the private sector partner under a PPP, we have provided a response when we considered the appreciation of inherent and contingent risks.

In terms of the analysis and development of PSC costs, from the review documents we identified the following facts:

• The development of the PSC had three distinct stages where costs were reviewed and changed;

Changes to the PSC - Three Stages | ||

Planned review in March/April 2013 | A second review in August 2013 mid-way through the RFP phase | |

• The 2012 DBC was prepared in a relatively short period of time between August 2012 and September 2012, following a Ministerial direction in August 2012 to consider PPP delivery for TG;

• The 2012 DBC version of the PSC was based on a 2011 version of Waka Kotahi's "Scheme Estimate" costing of risk-adjusted construction costs - this 2011 Scheme Estimate was based on the consented scheme estimate developed for the BOI's consideration. These facts meant the 2012 PSC was based on a consented scheme design developed using a non-PPP approach;

• The TGP's commercial/financial adviser and cost adviser played key and substantive roles in developing a risk- adjusted PSC using the 2011 Scheme Estimate costs and developing initial estimates of the risk adjustments required for a PSC;

• A Service Need Specification was not done for the DBC. The 2009 New Zealand PPP Guidelines, at pages 4 and 5 respectively, note the service need is a precedent step to development of the business case and is, "...the first and most critical step in the lifecycle of any procurement project is the articulation of the service need in functional terms.";

• The PSC assumed construction works would be procured under Waka Kotahi's traditional design and construct model contract (which includes a competitive bidding process);

• Waka Kotahi advised the Board in December 2012 that the 2012 DBC's PSC would be subject to a parallel estimate (cost) review, and that there was strong possibility that the parallel estimate may be different to the scheme estimate. Also, the Board was advised that the parallel estimate review was to ensure that the PSC estimate was as robust as possible;

• The first review of the PSC in March/April 2013 was informed by an independent cost review. This independent cost estimate was based on the 2011 Scheme Design and schedule of quantities. In summary, the construction cost increased by $77 million (or 12 percent) with the following major cost line changes:

March/April 2013 Review of the PSC - Major Cost Line Changes |

Environmental, earthworks and ground improvement |

Pavements |

Bridges |

Retaining Walls |

Services Relocations |

Weigh Stations and Weather Stations |

Interchanges and Link Roads |

• This upward change in the PSC's construction cost is summarised in Figure 3 (below):

Figure 3: March/April 2013 Review of the PSC - Main Changes

• In this first PSC review, the separate risk allowance contingencies for site, design and construction risks and O&M risks were decreased by $53 million and $14 million respectively. Our understanding from the review documents is this change appears to mainly reflect more certainty reflected through the increase in construction and O&M cost estimates.

• The TGP's commercial/financial adviser incorporated the above capital cost changes into a revised PSC (and consequently a revised AT), summarising, ".the (PSC) update involved estimation of current prices and quantities based on the scheme design. Therefore, while the process is referred to as an update, it is more accurately a re-estimation.".

• O&M costs were also included in the scope of 2013 review of the PSC. These O&M costings assumed the TG network was costed as part of a wider state highway network, i.e. was costed on a marginal basis, rather than as a discrete stand-alone project. This was explained as being consistent with the way in which the Waka Kotahi would manage the O&M portion of the TGP;

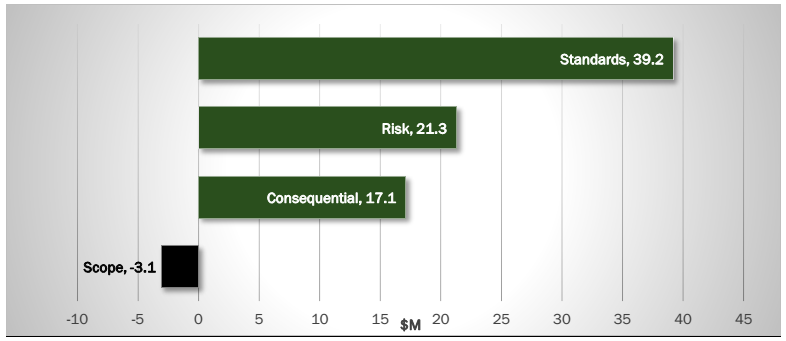

• The second review of the PSC was considered by the Waka Kotahi Board in August 2013 (mid-way through the RFP phase) and took into account changes related to: (i) the results of geotechnical investigations; (ii) application of RONS standards and a 110 km/hr design speed; and (iii) release (by Waka Kotahi) of a revised Bridge Manual. Another independent cost review was done of the PSC at this time and reported the following:

- "...Differences between the requirements prescribed in the PPP RFP and those of the Consented Design have been identified and highlighted during the IPP process and as a consequence, questions have been raised by the tenderers regarding the level of the AT; and

- The (independent cost advisor) endorses the conclusion that there are significant differences between the basis of the 'consented design' and those of the PPP RFP, which in aggregate add significantly to the Base Estimate. These differences relate to increases in a variety of standards; geotechnical information showing worse than previously assumed assumptions; and some added work scope.".

• These major cost line changes (total of $74.5 million) in the August 2013 review of the PSC are summarized below.

Figure 4: Second Review of the PSC (Aug 2013) - Main Changes

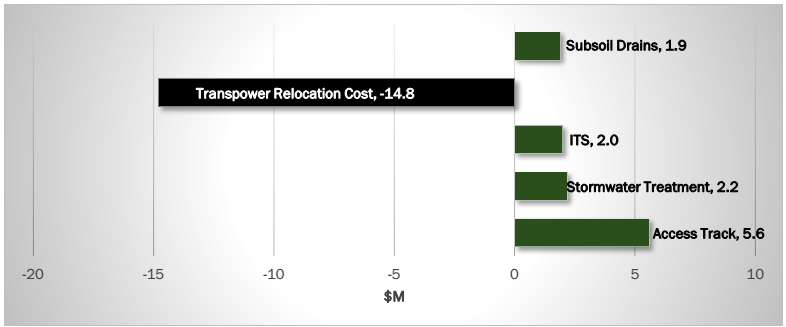

Figure 5: Breakdown of scope changes from Second Review of the PSC (Aug 2013)

| August 2013 Review of the PSC - Major Cost Line Changes |

Standards | • Changes related to design speed of 110kph compared to 100kph in the consented design • RFP prescribed median and shoulder widths significantly greater than for the consented design • Side protection barriers over clear zones • Revised Waka Kotahi Bridge Manual and Road Safety Audit requirements • Increased mitigation resulting from the increase in length of stream diversions • Required changes to the configuration/layout of interchanges • Additional earthworks for slopes greater than 30 metres |

Scope | Net impact of cost changes related to: • Access track included in RFP but not in 'consented design' schedule • Allowance for extra stormwater treatment • Increased provision for VMS; traffic monitoring and CCTV • Reduction in Transpower relocation cost plus associated costs • Allowance for subsoil drains full length under pavement |

Risk | • Changes in risk contingency related to changes in Road Safety Audit requirements • Changes in risk contingency related to changes in Geotechnical requirements, comprising: - investigation results identified conditions worse than previously thought, particularly at Wainui Saddle and some bridge sites, in particular Cannons Creek - liquefiable materials identified at SH58 and Mackays Crossing - investigation results indicated cut to fill materials wetter than previously assumed - revised Bridge Manual required additional seismic performance related design for bridges, particularly at abutments. |

Consequential | • Changes in design fee estimate to reflect additional geotechnical design and monitoring input required |

• In the August 2013 briefing paper to the Board, Waka Kotahi also provided the following advice:

- When approving the use of the PPP model in Oct 2012, the Board was advised that the estimate for the TGP was based on the Consented Scheme Design. Normal practice for Waka Kotahi is to finalise the funding envelope for a project at the Design Estimate phase, which in general is at a significantly more developed stage than the Consented Scheme phase.

- This difference in accuracy is because with the additional design completed at the Design Estimate phase, a better understanding of scope and risk allows a more accurate reflection of the project cost and less reliance on risk assessments.

- As such for the TGP, Waka Kotahi has been carrying the risk of the estimate being less accurate than would normally be the case when a funding decision is made. While this would be an issue under either a traditional or PPP procurement, for a PPP the reliance on an accurate estimate is also of critical importance in the demonstration of value for money.

- The timing of the PSC review was established to provide: (i) Waka Kotahi with increased confidence in the PSC, similar to what would be achieved at the Design Estimate phase; (ii) the most accurate estimate to effectively implement the value for money test for the PPP: and (iii) provide the PPP Respondents sufficient time to reflect in their proposals thus providing the best opportunity for them to provide a value for money solution.