6.5 Lender approval process

Where the senior lender remains an active party on a project, there will be a requirement to seek the approval of the lender or the lending group. In some cases, the Loan or Facilities Agreement may have a threshold for Change Orders to require Lender Approval and, should this not be breached, then the Borrower and the Authority can agree and approve the changes requirement without needing recourse to Lender engagement. It should be noted that these thresholds can be quite low and it is likely that the majority of NZ strategies would fall above the threshold.

However, the rise of ESG Reporting and the interest in green investment should increasingly push lenders in the direction of NZ funding opportunities.

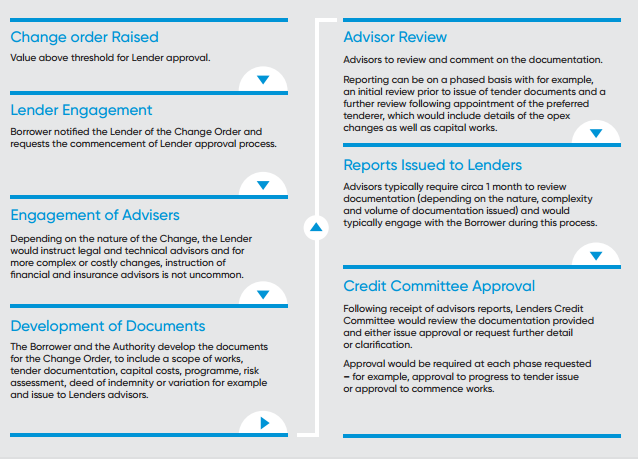

Whilst the specific processes for credit approval of change will vary between lenders, the typical process is demonstrated below:

Figure 7 |

|

Depending on the complexity of the change request, the process can be lengthy. It is not uncommon for approval to be required for larger changes at different stages of the process. For example, approval to issue tender documentation, approval of the preferred tenderer documentation and final approval which will require any changes to the unitary payment and any payment mechanism re-calibration to be completed.

Some lenders may be content with an initial Letter or Deed of Indemnity to allow works to commence, whilst the final Supplemental Agreement is being prepared, which can enable the initial approval to be granted at an earlier stage. Noting this, lenders will require advisor review of all final documents prior to sign off.